A Realistic, Step-by-Step Guide to Taking Back Control of Your Money

Why It Feels Impossible to Get Ahead

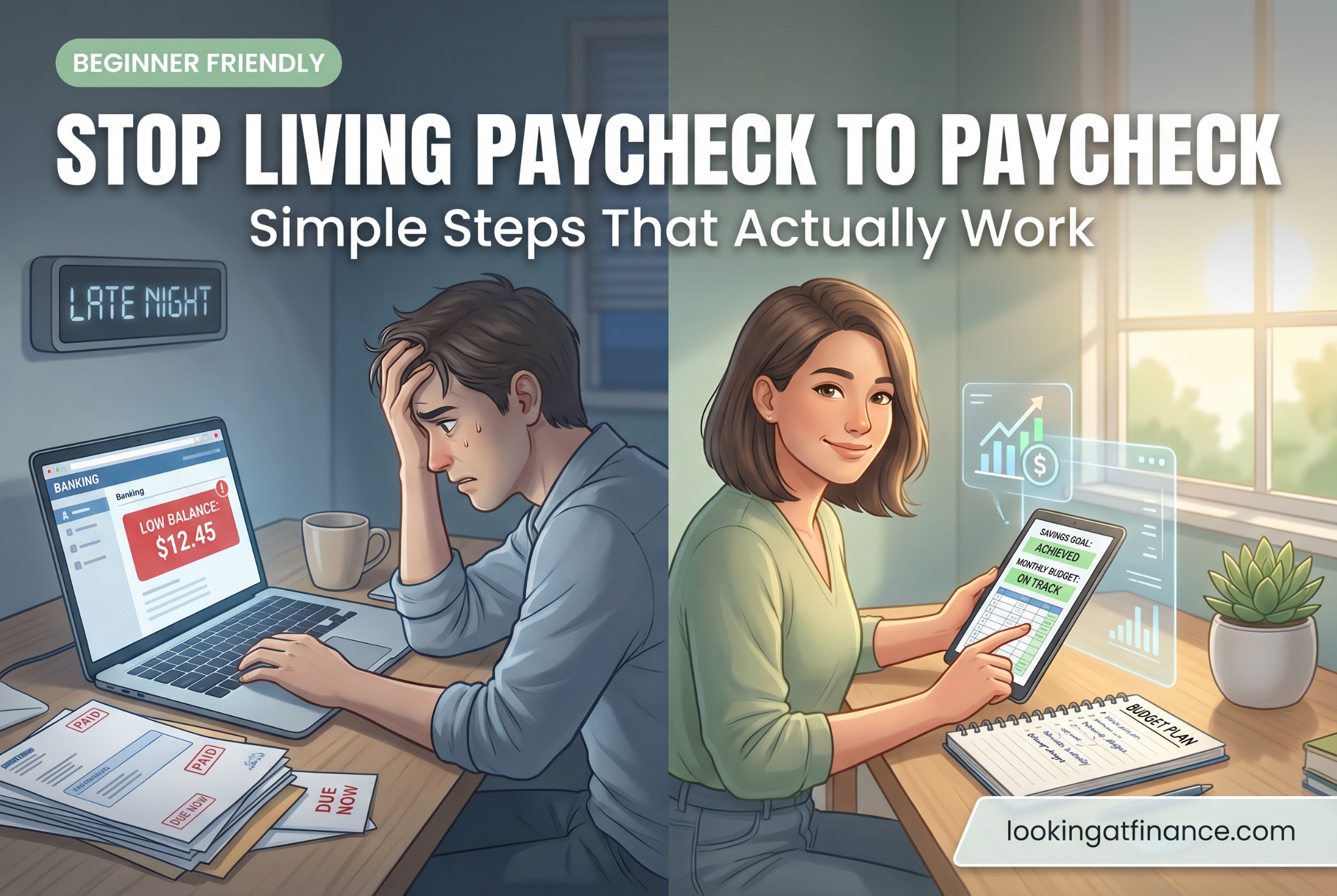

Living paycheck to paycheck is exhausting.

You get paid…

You pay bills…

And then there’s nothing left.

No savings.

No breathing room.

No margin for mistakes.

And over time, it starts to feel like:

- “No matter what I do, I can’t get ahead.”

- “I’m always starting over.”

- “Something always comes up.”

If that sounds familiar, you’re not alone.

This is how millions of people live—not because they’re careless, but because they don’t have a clear system.

👉 And that’s what this article will fix.

What “Paycheck to Paycheck” Really Means

Living paycheck to paycheck doesn’t always mean you’re broke.

It usually means:

- Your income covers your expenses—but barely

Most of your money goes toward bills and essentials, leaving little room for flexibility or saving. - There’s little or nothing left after bills

Once expenses are paid, your account is nearly empty, making it hard to prepare for future needs. - One unexpected expense can throw everything off

A small emergency like a repair or medical cost can disrupt your entire budget and create stress. - You rely on the next paycheck to survive

Your financial stability depends on your next income, with little or no buffer to fall back on.

👉 The real issue isn’t just income—it’s lack of control

Why People Stay Stuck in This Cycle

Before you fix the problem, you need to understand it.

Many people repeat the same money habits without realizing it, making it harder to break the cycle. Identifying the root causes helps you make better decisions and create lasting financial change.

1. No Clear Plan

Most people don’t have a system for their money.

They:

- Spend first

Money is used as soon as it comes in, often on immediate needs or impulse purchases without thinking about priorities. - Adjust later

After spending, you try to manage what’s left, often leading to stress, missed payments, or running out of money.

👉 That approach keeps you stuck

2. Small Expenses Add Up

It’s not always big spending.

It’s:

- Daily snacks

Small purchases like drinks or snacks seem minor but add up over time, taking a noticeable portion of your monthly budget. - Random purchases

Unplanned buying, especially online or in stores, can quickly increase spending without you realizing how much you’re using. - Subscriptions

Monthly services may feel affordable individually, but combined, they reduce your available money for more important expenses.

👉 These quietly drain your income

3. No Savings Buffer

Without savings:

- Every problem becomes urgent

Even small issues like a repair or bill increase must be handled immediately, often forcing you to borrow money or delay other payments. - Every expense feels stressful

Without a financial cushion, normal costs can feel overwhelming, making it harder to stay calm and make clear decisions.

👉 You’re always reacting

4. Income Limits

Sometimes, your income simply isn’t enough.

And while budgeting helps:

- Limited earning power

Your current income may only cover basic needs, leaving little room to save or handle unexpected expenses. - Higher cost of living

Expenses like rent, food, and transport can take up most of your income, making it harder to stay balanced financially.

👉 Income still matters

Step 1: Know Exactly Where Your Money Is Going

You cannot fix what you don’t see.

Most people feel broke—but don’t actually track their money.

Without tracking, it’s easy to miss where your money is going, especially with small daily spending. Writing everything down helps you see patterns and identify areas where you can improve.

What You Need to Do

Write down:

- Your income

Record all the money you receive so you know exactly how much you have available to work with each month. - Your expenses

List all your regular costs, including bills and daily spending, to understand where your money is going. - Every dollar you spend

Track even small purchases, as they add up over time and can reveal patterns you may not notice otherwise.

Why This Matters

This helps you:

- Identify waste

You can see where money is being spent unnecessarily, allowing you to cut back on expenses that don’t add real value. - Spot patterns

Tracking reveals habits like frequent small purchases or overspending in certain areas, helping you make better decisions. - Understand your real situation

You get a clear picture of your finances, making it easier to plan and improve your money management.

👉 Awareness is the first step to control

Step 2: Build a Survival Budget (Keep It Simple)

When money is tight, you don’t need a perfect budget.

You're already investing time in improving your finances, and that's something to be proud of. Before you continue, download our free 7 Days To Financial Clarity™ workbook and start putting these ideas into action.

You need a working budget.

A simple plan focused on essential expenses helps you stay stable and avoid confusion. By keeping your budget realistic and easy to follow, you’re more likely to stay consistent and make progress over time.

Use 3 Categories

- Needs (60–70%)

Covers essential expenses like housing, food, and transport, helping you maintain stability and meet your basic daily living requirements. - Obligations (20–30%)

Includes required payments such as debt and bills that must be paid regularly to avoid penalties or added financial stress. - Savings (even 1–10%)

Sets aside a small portion for emergencies or future needs, helping you gradually build financial security over time.

Why This Works

- It removes overwhelm

By focusing on just a few categories, you avoid confusion and make budgeting feel easier to manage from the start. - It simplifies decisions

You can quickly decide where your money should go without overthinking every expense or second-guessing your choices. - It helps you focus on what matters

Your attention stays on essential spending, required payments, and saving, helping you build stability and improve your financial situation.

Step 3: Cut “Silent Money Leaks”

Most people don’t realize where their money is going.

Small, repeated purchases often go unnoticed, but over time they reduce how much money you have available. Identifying and cutting these expenses helps you free up money without making major lifestyle changes.

Common Money Leaks

- Daily snacks or drinks

Small daily purchases like coffee or snacks seem harmless but can add up quickly over a month. - Subscriptions you forgot about

Ongoing payments for unused services continue to charge you, reducing your available money without providing real value. - Small online purchases

Frequent low-cost items can accumulate over time, often without you noticing how much you’ve spent. - Convenience spending

Paying extra for convenience, like takeout or ride services, increases costs compared to more affordable options.

Real Example

$5 per day =

👉 $150 per month

👉 $1,800 per year

That’s not small.

What to Do

- Track spending for 3 days

Write down every purchase, including small ones, to see exactly where your money is going over a short period. - Identify 2–3 things to cut

Look for expenses you can reduce or remove without affecting your basic needs or daily responsibilities. - Start there

Focus on making a few simple changes first instead of trying to fix everything at once.

👉 Small changes create big results

Step 4: Prioritize Needs Over Wants

When money is tight, clarity matters.

Focusing on essential expenses first helps you stay stable and avoid financial stress. By clearly separating needs from wants, you make better decisions and ensure your money is used where it matters most.

Simple Rule

👉 If you can live without it temporarily, it’s not a need

This helps you quickly decide what to prioritize when money is limited. If an expense can be delayed or reduced without affecting your basic living, it can be treated as a want and adjusted to fit your budget.

Real-Life Shift

- Buying lunch daily → Cooking simple meals

Preparing food at home reduces daily spending while still meeting your needs, helping you save money without sacrificing nutrition. - Multiple subscriptions → Keeping one

Limiting subscriptions to only what you actually use helps reduce unnecessary expenses and frees up money for more important financial priorities.

👉 These decisions create financial space

Step 5: Plan Your Money Before You Spend It

This is one of the biggest mindset shifts.

Deciding where your money should go before spending helps you stay in control and avoid running out of money. Planning ahead ensures your needs and priorities are covered first, reducing stress and improving financial stability.

Most People Do This:

Spend → then budget

Understanding money is one thing. Seeing your own numbers is where real financial progress begins. Spend one minute using our free Budget Calculator and discover where your money can work harder for you.

What Works:

👉 Plan → then spend

- Set priorities first

Decide how your money will be used for needs, bills, and savings before spending anything else. - Give every dollar a purpose

Assign your income to specific categories so you know exactly where it should go. - Spend what’s left

Use the remaining money for flexible expenses, helping you stay within your budget and avoid overspending.

Simple System

When you get paid:

- Cover your needs

Pay essential expenses like rent, food, and utilities first to ensure your basic living requirements are secured. - Set aside savings

Put aside a small amount immediately, even if it’s minimal, to start building financial stability and a safety buffer. - Spend what’s left

Use the remaining money for flexible expenses, helping you stay within limits and avoid overspending.

👉 This gives every dollar a purpose

👉 If you’re living paycheck to paycheck, this step-by-step method can help you regain control of your money.

Step 6: Use Visual Spending (Cash or Limits)

When money is invisible, it’s easy to overspend.

Using cash or setting clear limits makes your spending more visible, helping you stay aware of how much you have left and avoid going over your budget.

Why Cash Works

- You see it

Physically seeing your money decrease makes you more aware of how much you’re spending and what you have left. - You feel it

Handing over cash creates a stronger connection to your spending, making you think twice before buying. - You control it

Once your cash is gone, you naturally stop spending, helping you stay within your budget limits.

Try This

- Withdraw money for food/transport

Take out a set amount in cash for essential categories so you can clearly manage and limit your spending. - Use envelopes or categories

Separate your cash into labeled groups, helping you organize your money and avoid mixing funds for different expenses. - Stop when it’s gone

When the allocated money runs out, you pause spending, which prevents overspending and keeps you within your budget.

👉 This creates discipline automatically

Step 7: Build a Small Emergency Fund

Even if you’re broke—you need a buffer.

Setting aside even a small amount helps you handle unexpected expenses without relying on debt, reducing stress and giving you more control over your financial situation.

Start Small

- $50

Begin with a small, realistic amount that you can save quickly, giving you an immediate sense of progress and motivation. - $100

Building toward a slightly larger goal helps strengthen your habit and provides a better cushion for minor unexpected expenses. - Then grow

Continue increasing your savings over time as your situation improves, creating a stronger financial buffer for future needs.

Why This Matters

Without savings

👉 Every problem becomes a crisis

Even small expenses like repairs or bills must be handled immediately, often forcing you to borrow or delay other important payments.

With savings

👉 You have options

Having a financial buffer allows you to handle unexpected costs calmly, avoid debt, and make better decisions without pressure.

Step 8: Increase Your Income (Even Slightly)

Budgeting alone has limits.

At some point:

👉 Income matters

- Budgeting stretches what you have

Managing your money helps, but it can only go so far if your income stays the same. - Extra income creates breathing room

Even small increases can help cover expenses, build savings, and reduce financial pressure.

Start Small

You don’t need a new career.

Try:

- Selling unused items

Turn things you no longer use into extra cash, helping you free up space and increase your income at the same time. - Small side jobs

Take on simple tasks like deliveries or short-term work to earn additional money without long-term commitment. - Helping others for pay

Offer basic services like cleaning or errands to people nearby, creating opportunities to earn extra income quickly.

Why This Helps

Even:

👉 $50–$100 extra/month

Every financial journey is different. Take our free Financial Goal Assessment to discover which area deserves your attention first and receive a clear direction for your next financial milestone.

Can:

- Cover a bill

Extra income can help pay small expenses like utilities or transportation, reducing pressure on your main income. - Build savings

Setting aside even a portion of this money helps you grow a financial cushion over time. - Reduce stress

Having additional income provides relief, making it easier to manage your finances without constant worry.

Step 9: Avoid the “I Deserve This” Trap

When life is hard, spending feels like relief.

That’s normal.

But it can keep you stuck.

- Emotional spending feels rewarding

Buying something can provide short-term comfort, especially after a stressful day or situation. - It creates a repeating cycle

Temporary relief leads to more spending, which can worsen your financial situation over time. - It delays real progress

Money used for impulse spending could be saved or used to improve your financial stability.

Real Pattern

You’re stressed → you spend → you feel better → repeat

The Problem

- It feels good short-term

Spending can give immediate satisfaction or relief, making it seem like a quick solution to stress or frustration. - But changes nothing long-term

The temporary feeling fades, while your financial situation remains the same or becomes more difficult to manage over time.

Better Approach

👉 Find free ways to reward yourself

- Rest

Taking time to relax helps you recover mentally and physically, reducing stress without spending money and improving your overall well-being. - Walk

A simple walk can clear your mind, improve your mood, and provide a healthy break without any cost. - Time with family

Spending quality time with loved ones builds connection and happiness without relying on spending for enjoyment. - Simple hobbies

Activities like reading, journaling, or listening to music provide entertainment and satisfaction without adding financial pressure.

Step 10: Stay Consistent (This Is Everything)

Budgeting is not a one-time fix.

It’s a habit.

- Progress happens over time

Small, repeated actions like tracking spending and saving regularly lead to real financial improvement. - Consistency builds stability

Following your budget consistently helps you stay in control and avoid falling back into old habits. - Mistakes are part of the process

Missing your budget occasionally is normal—what matters is getting back on track and continuing forward.

What to Expect

- Mistakes

You may overspend or forget to track certain expenses at times, which is part of learning how to manage your money better. - Unexpected expenses

Costs like repairs or emergencies can come up suddenly, testing your budget and requiring quick adjustments. - Frustration

Changing money habits can feel difficult at first, especially when progress seems slow.

👉 That’s normal

What Matters

👉 Restart quickly—not perfectly

Real-Life Example (Simple Breakdown)

Let’s say:

You save:

- $2 per day

That’s:

- $60 per month

- $720 per year

Add small cuts:

👉 $1,000+ saved

👉 That’s how change happens

Common Mistakes to Avoid

1. Waiting Until You Earn More

Start with what you have.

Delaying action keeps you in the same financial situation. Even with a low income, small changes like tracking spending or saving a little can create progress and help you build better money habits over time.

2. Trying to Be Perfect

Consistency matters more.

Trying to follow a perfect plan can feel overwhelming and lead to giving up. Focusing on small, consistent actions helps you build habits and make steady progress without unnecessary pressure.

3. Ignoring Small Spending

It adds up fast.

Small daily purchases may seem harmless, but over time they can take a significant portion of your income. Paying attention to these expenses helps you control your spending and improve your overall budget.

4. Giving Up Too Soon

Progress takes time.

Improving your financial situation doesn’t happen overnight. It requires consistent effort and patience. Even small steps, repeated over time, lead to meaningful results, so staying committed is more important than expecting quick changes.

How Your Life Changes When You Break the Cycle

This is bigger than money.

Breaking the paycheck-to-paycheck cycle improves your mindset, reduces stress, and gives you a sense of stability. It affects how you make decisions, plan your future, and handle challenges with more confidence and control.

1. Less Stress

You stop feeling overwhelmed.

With a clear plan for your money, you no longer worry constantly about bills or running out of cash. This reduces daily pressure and helps you feel more calm and in control.

2. More Confidence

You believe:

👉 “I can manage this”

As you follow your plan and see progress, you begin to trust your decisions. This confidence helps you stay consistent, make better financial choices, and handle challenges without feeling stuck or uncertain.

3. More Freedom

Even small savings create options.

Having money set aside gives you the ability to handle situations without stress, make choices without pressure, and avoid depending on debt, giving you more control over your financial life.

4. More Control

You stop reacting—and start planning.

With a clear budget and savings, you begin to make decisions ahead of time instead of responding to problems. This helps you stay organized, avoid surprises, and move toward your financial goals with more confidence.

👉 This isn’t about being perfect—it’s about making progress.

Final Thoughts: You’re Not Stuck—You’re Starting

If you’re living paycheck to paycheck:

That doesn’t mean you’re failing.

It means you haven’t had the right system—yet.

With the right approach, small changes can lead to real progress over time, helping you move from surviving to gaining control and building a more stable financial future.

Remember This

👉 You don’t need more money to start

👉 You need a simple plan

Start Today

- Track your spending

Write down everything you spend so you can clearly see where your money is going and identify areas to improve. - Cut one expense

Choose one small cost you can reduce or remove to immediately create extra space in your budget. - Save something small

Set aside even a tiny amount to start building the habit and create progress over time.

👉 That’s how real change begins

FAQs

How do I stop living paycheck to paycheck fast?

Focus on cutting small expenses, creating a simple budget, and increasing income slightly. Small consistent changes add up quickly.

Start by identifying unnecessary spending, organizing your money into clear categories, and finding ways to earn even a little extra. These steps create immediate improvements and build momentum over time.

Is it possible to save money on a low income?

Yes. Even small amounts like $1–$5 regularly can build over time and improve your financial stability.

Saving small amounts consistently helps you build the habit and create progress, even with limited income. Over time, these small savings add up and provide a buffer for unexpected expenses.

What is the fastest way to break the cycle?

Tracking spending and cutting unnecessary expenses immediately creates the fastest impact.

By seeing exactly where your money is going, you can quickly remove or reduce non-essential spending, creating extra space in your budget and improving your financial situation right away.

Do I need a high income to stop struggling?

No. While income helps, better money management and consistency are what create long-term change.

Even with a modest income, tracking your spending, reducing unnecessary expenses, and saving small amounts regularly can improve your situation and help you build financial stability over time.

You have invested time learning today. Now take the next step by downloading our free 7 Days To Financial Clarity™ workbook and begin building a stronger financial future.