A Simple, Real-Life Guide to Managing Your Money Without Feeling Overwhelmed

Why Budgeting Feels So Confusing

Budgeting sounds simple… until you try to do it.

There are too many methods.

Too many rules.

Too many opinions.

And if you’re just starting, it can feel like:

- “Where do I even begin?”

- “Am I doing this right?”

- “Why does this feel so complicated?”

For many people, budgeting becomes something they avoid—not because they don’t care, but because it feels overwhelming.

That’s where the 50/30/20 budget rule comes in.

It simplifies everything.

Instead of tracking dozens of categories, you divide your money into just three parts.

👉 That’s it.

No complicated systems.

No confusion.

Just a clear starting point that actually works.

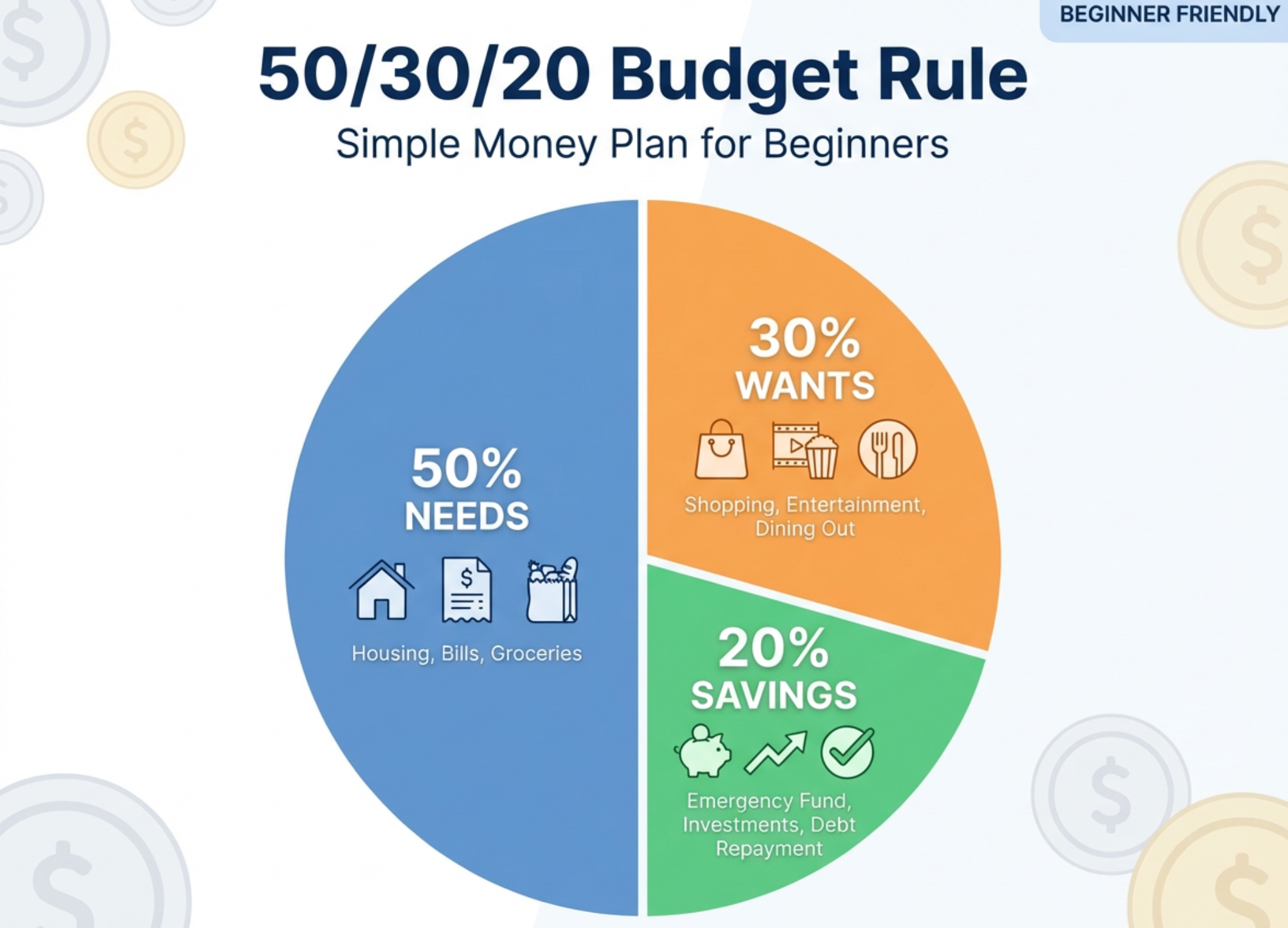

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting method that divides your income into three categories:

- 50% → Needs

This portion covers essential living expenses like rent, groceries, transportation, and utilities—costs you must pay to maintain your basic daily life and stability. - 30% → Wants

This includes non-essential spending such as eating out, entertainment, or shopping—things that improve your lifestyle but can be reduced if necessary. - 20% → Savings and Debt

This portion goes toward building your financial future, including saving money, paying off debt, and creating a safety net for unexpected expenses.

Each percentage represents how much of your income should go toward that category, helping you balance living expenses, lifestyle choices, and future financial security.

Why This Budget Rule Works (Especially for Beginners)

Most people don’t fail at budgeting because they’re careless.

They fail because the system is too complicated.

The 50/30/20 rule works because:

- It’s easy to understand

With only three categories, you don’t have to track dozens of expenses, making it simple to follow even if you’re completely new to budgeting. - It’s flexible

You can adjust the percentages based on your income and situation, allowing the method to work whether you’re earning a little or a lot. - It reduces decision fatigue

Instead of constantly wondering if you can afford something, you already know which category it belongs to, making spending decisions quicker and clearer. - It’s realistic for everyday life

It allows room for both essentials and enjoyment, so you can manage your money without feeling restricted or overwhelmed.

Instead of asking:

👉 “Where did my money go?”

You start asking:

👉 “Where should my money go?”

That shift changes everything.

Step 1: Know Your Real Income (Start Here)

Before you can budget anything, you need one number:

👉 Your monthly take-home income

This is the money you actually receive after taxes—not your full salary.

If your paycheck shows $1,200 but you only receive $1,000 after deductions, your budget must be based on the $1,000. Using the correct number helps you avoid overspending, plan accurately, and create a budget that actually works in real life.

What to Include

- Salary or wages

This is your main income from your job, whether paid weekly or monthly, and it forms the foundation of your budget and financial planning. - Side income

Include any extra earnings from small jobs, freelance work, or selling items, even if it varies, so you have a more complete picture of your income. - Any consistent support

Money received regularly from family, government programs, or assistance should be included, since it contributes to what you can actually spend and manage each month.

Why This Matters

If you budget based on money you don’t actually have, your plan will fail.

Using your real income ensures your budget is:

- Accurate

Your numbers reflect what you truly have available, helping you avoid mistakes like overspending or underestimating your expenses. - Sustainable

You can maintain your budget over time because it’s based on realistic income, not expectations that may change or fall short. - Practical

Your budget works in real life, allowing you to pay bills, manage spending, and make decisions without constantly running into financial problems.

Step 2: Break Your Money Into 3 Simple Categories

Now you divide your income into three clear parts.

This is where the 50/30/20 rule becomes powerful.

Instead of tracking every single expense, you group your money into needs, wants, and savings. This makes budgeting easier to understand and manage, helping you quickly see where your money is going and where adjustments may be needed.

1. Needs (50%)

Your Essential Living Expenses

Needs are the expenses you must pay to live and function.

These include the basics required for daily survival, such as housing, food, transportation, and utilities. If these are not paid, your ability to live safely or earn income is affected. Keeping this category within 50% helps you maintain stability while leaving room for other financial priorities.

You're already investing time in improving your finances, and that's something to be proud of. Before you continue, download our free 7 Days To Financial Clarity™ workbook and start putting these ideas into action.

What Counts as a Need

- Rent or mortgage

This is your housing cost and must be paid consistently to maintain a safe place to live, making it one of your highest financial priorities. - Basic groceries

These are essential food items needed for daily nutrition, and planning simple meals helps keep this expense within your budget. - Transportation

Costs like bus fare or fuel are necessary to get to work or handle daily responsibilities, directly supporting your ability to earn income. - Utilities (electricity, water, phone)

These services keep your home functional and allow you to stay connected, making them essential for both daily living and communication. - Insurance

Payments for health, car, or other coverage protect you from large unexpected expenses, helping prevent financial setbacks during emergencies.

Simple Rule

👉 If you don’t pay it, your life becomes unstable

This helps you quickly identify true needs. Missing rent could lead to losing your home, and skipping utility payments could leave you without electricity or water. Focusing on these essential expenses first ensures your basic living conditions and daily responsibilities are protected.

Beginner Example

- Buying groceries → Need

Groceries provide the basic food you need to eat daily and maintain your health, making them essential for survival and part of your core living expenses. - Ordering fast food → Want

Fast food is convenient but not necessary, and choosing it often increases spending compared to cooking at home, making it a flexible expense you can reduce when needed.

Why This Category Matters

Needs usually take the largest portion of your income.

But here’s the important part:

👉 If your needs go above 50%, your budget becomes tight and stressful.

When most of your money goes toward essentials, there’s little left for savings or unexpected expenses. This can lead to constant pressure, making it harder to manage your finances or improve your situation over time.

Real-Life Scenario

- Monthly income: $1,200

This is your total take-home pay available for all expenses, meaning every dollar must be carefully planned to avoid running short. - Needs should be around: $600

Based on the 50% rule, this is the ideal amount to cover essential living expenses while leaving room for wants and savings. - If your rent alone is $700

Your housing cost already exceeds your needs limit, leaving less money for food, transport, and other essentials.

👉 You already have a problem to solve

This highlights a gap in your budget, showing that adjustments are needed to reduce expenses or increase income.

👉 This doesn’t mean failure—it means awareness

Seeing the issue clearly helps you make better decisions and take steps to improve your financial situation.

2. Wants (30%)

Your Lifestyle and Enjoyment

Wants are expenses that improve your life—but are not essential.

These are things you choose to spend money on for comfort, fun, or convenience. While they’re not required for survival, they help you enjoy your life and stay motivated. Managing this category properly allows you to enjoy spending without losing control of your budget.

What Counts as a Want

- Eating out

Meals from restaurants or fast food are convenient and enjoyable but usually cost more than cooking at home, making them optional rather than essential. - Entertainment

Activities like movies, events, or streaming services are for enjoyment and relaxation, but they are not necessary for daily living. - Subscriptions

Monthly services like streaming platforms or apps add convenience but can often be reduced or canceled if money is tight. - Shopping

Buying clothes, accessories, or non-essential items is based on preference, not necessity, and can be delayed when needed. - Travel

Trips and vacations provide experiences but are not required for daily life, making them flexible and adjustable expenses.

Important Truth

Wants are not bad.

They are part of a balanced life.

Enjoying your money in moderation helps you stay motivated and avoid feeling restricted. When you include reasonable wants in your budget, you’re more likely to stick to it long term instead of giving up or overspending later.

Why This Category Exists

If you remove all wants:

- You feel restricted

Cutting out all enjoyable spending can make your budget feel too strict, leading to frustration and making it harder to stick with over time. - You lose motivation

Without small rewards or enjoyment, budgeting can feel like a constant sacrifice, reducing your willingness to continue managing your money. - You stop budgeting

When a budget feels unrealistic, people often give up completely and return to unplanned spending habits.

This category allows you to enjoy life—without losing control, helping you stay consistent while still making progress financially.

Real-Life Example

- Buying coffee every day

Daily purchases may seem small, but over time they add up and can take a noticeable portion of your monthly budget. - Limit it to a few times per week

Reducing how often you spend allows you to enjoy the same habit while keeping your expenses under control.

👉 You still enjoy it—but within your budget

You don’t have to eliminate what you enjoy, just adjust it so it fits comfortably within your financial plan.

3. Savings and Debt (20%)

Your Future and Financial Growth

This is the most important category for long-term stability.

Understanding money is one thing. Seeing your own numbers is where real financial progress begins. Spend one minute using our free Budget Calculator and discover where your money can work harder for you.

It focuses on building financial security over time by saving money and reducing debt. While it may not feel urgent, consistently setting money aside helps you prepare for emergencies, avoid future stress, and create a more stable and secure financial situation.

What Goes Here

- Emergency savings

Money set aside for unexpected situations like medical expenses, repairs, or urgent bills, helping you handle problems without relying on debt or falling behind financially. - Debt repayment

Payments toward loans or credit cards reduce what you owe over time, helping you avoid high interest and improve your overall financial position. - Investments

Money used to grow your wealth over time, such as savings accounts or long-term plans, helping you build financial security for the future.

Why This Matters

Without savings:

👉 Every unexpected expense becomes a problem

Even small issues like a repair or medical cost can force you to borrow money or delay important bills, creating added stress and financial pressure.

Without debt repayment:

👉 You stay stuck financially

Ongoing interest and unpaid balances keep increasing what you owe, making it harder to move forward or build any meaningful financial progress over time.

Beginner Tip

If 20% feels impossible:

👉 Start smaller

Begin with an amount you can manage consistently, even if it feels small, so you build the habit without overwhelming your budget.

Even:

- 5%

Setting aside a small portion of your income helps you start saving while still covering your essential expenses. - 10%

A slightly higher amount can speed up your progress, helping you build savings or reduce debt more effectively over time.

👉 Still moves you forward

Any amount saved or used to reduce debt creates progress, making your financial situation more stable step by step.

Step 3: Apply the 50/30/20 Rule (Simple Example)

Let’s make this practical.

Start by taking your monthly income and dividing it into the three categories—needs, wants, and savings. This helps you clearly see how much you can spend in each area, making your budget easier to follow and adjust based on your real financial situation.

Example Budget

Monthly income: $1,000

- Needs → $500

- Wants → $300

- Savings → $200

What This Does

You now have:

- A clear plan

You know exactly how your money should be divided, making it easier to manage your income without confusion or uncertainty. - Defined limits

Each category has a set amount, helping you control spending and avoid going over budget in any area. - Less stress

Having a structured plan reduces financial anxiety because you understand where your money is going and what to expect.

👉 No more guessing

You make decisions based on a clear system, not assumptions, giving you more confidence and control over your finances.

What If Your Budget Doesn’t Fit the 50/30/20 Rule?

This is very common—especially for beginners.

Your income, expenses, or financial situation may not match the ideal percentages right away. That’s normal. The goal is not to fit perfectly into the rule, but to use it as a guide to understand where your money is going and where you can improve over time.

Situation 1: Your Needs Are Too High

Example:

Needs = 70–80%

- Housing takes up most of your income

High rent or mortgage payments can consume a large portion of your earnings, leaving little room for other essential expenses. - Basic living costs are higher than expected

Expenses like groceries, utilities, and transportation may cost more than anticipated, especially with rising prices. - Limited flexibility in your budget

With most of your income going toward needs, it becomes difficult to save, handle emergencies, or adjust spending without financial strain.

Why This Happens

- High rent

Housing costs often take up a large portion of your income, especially in expensive areas, leaving less money available for other essential expenses. - Low income

When earnings are limited, even basic needs can consume most of your budget, making it harder to balance spending and save. - Limited flexibility

Fixed expenses like rent and utilities cannot be easily reduced, making it difficult to adjust your budget without changing your income or living situation.

What You Can Do

- Look for ways to reduce expenses

Review your spending and identify areas where you can cut back, such as lowering utility usage or choosing more affordable options for everyday needs. - Adjust spending habits

Small changes, like cooking at home instead of eating out, can free up money and help you better manage your budget. - Increase income (even slightly)

Earning extra money through small jobs or side activities can help cover gaps and make your budget more manageable.

👉 Even small changes help

Situation 2: You Can’t Save 20%

This is normal.

If your income is limited or your expenses are high, setting aside 20% may feel unrealistic at first. Many beginners face this situation, and it doesn’t mean you’re doing anything wrong—it simply reflects your current financial reality and the need to start gradually.

Every financial journey is different. Take our free Financial Goal Assessment to discover which area deserves your attention first and receive a clear direction for your next financial milestone.

What to Do Instead

- Start with 1–5%

Begin by saving a small portion of your income that feels manageable, so you can build the habit without putting pressure on your budget. - Build gradually

Increase your savings slowly over time as your income improves or expenses decrease, making the process more realistic and sustainable. - Focus on consistency

Saving regularly, even small amounts, helps you build progress and creates a stable financial habit that grows over time.

👉 Progress matters more than perfection

How to Adjust the Rule for Your Reality

The 50/30/20 rule is not strict.

It’s a guideline.

If You’re Living Paycheck to Paycheck

- 70% Needs

A larger portion of your income goes toward essential expenses like rent, food, and transport, reflecting the reality of limited financial flexibility. - 20% Wants

You still allow some room for personal spending, but keep it controlled to avoid overspending and maintain balance. - 10% Savings

Even a small percentage helps you start building financial security, creating a foundation for future stability over time.

If You Have Debt

Try:

- 50% Needs

Keep essential expenses within half of your income so you can cover basics like housing, food, and utilities without overwhelming your budget. - 20% Wants

Limit lifestyle spending to a smaller portion, allowing enjoyment while staying focused on improving your financial situation. - 30% Debt/Savings

Allocate a larger share toward paying off debt or building savings, helping you reduce financial pressure faster and create long-term stability.

👉 Adjust based on your situation—not someone else’s

Common Mistakes Beginners Make

1. Trying to Be Perfect

- A perfect budget doesn’t exist

Your income, expenses, and priorities will change, so expecting everything to be exact every month can lead to frustration and unrealistic expectations. - 👉 A working budget does

Focus on creating a plan you can follow consistently, even if it’s not perfect, because steady progress is what improves your financial situation over time.

2. Ignoring Small Spending

Small purchases feel harmless—but they add up fast.

Daily expenses like snacks, drinks, or small online purchases may seem insignificant, but over time they can take a noticeable portion of your income. Tracking these costs helps you see patterns and make small adjustments that improve your overall budget.

3. Not Tracking Money

If you don’t track it:

👉 You lose control of it

Without tracking your spending, it becomes difficult to understand where your money is going. This can lead to overspending, missed opportunities to save, and financial stress, making it harder to stay within your budget and improve your situation over time.

4. Giving Up Too Soon

Budgeting is a habit—not a quick fix.

Mistakes are part of the process.

It takes time to adjust your spending, learn your patterns, and build consistency. Missing your budget one week or making a mistake doesn’t mean failure—it’s part of learning. Sticking with it over time is what leads to real financial improvement.

How to Make the 50/30/20 Rule Work in Real Life

1. Start Simple

Don’t overcomplicate it.

Focus on dividing your income into the three main categories without worrying about perfect details. Trying to track everything at once can feel overwhelming, so keeping it simple helps you stay consistent and actually follow your budget over time.

2. Track Your Spending Weekly

This helps you stay aware and adjust quickly.

Checking your spending once a week allows you to catch problems early, such as overspending in one category. This makes it easier to correct your habits before the end of the month and stay within your budget.

3. Adjust Monthly

Your situation will change.

Your budget should too.

Expenses, income, and priorities can shift from month to month, so reviewing your budget regularly helps you stay aligned with your current reality. Making small adjustments ensures your budget continues to work effectively instead of becoming outdated or unrealistic.

4. Be Honest With Yourself

Budgeting only works when you’re realistic about your habits.

If you underestimate your spending or ignore certain expenses, your budget won’t reflect reality. Being honest about where your money goes helps you make better decisions, adjust your plan, and create a budget you can actually follow consistently.

Real-Life Scenario (Beginner Friendly)

Let’s say:

You earn $800/month.

Your Budget

- Needs → $480

- Wants → $240

- Savings → $80

What Happens Over Time

- You reduce small expenses

As you become more aware of your spending, you naturally cut back on unnecessary purchases, freeing up money without making drastic lifestyle changes. - You build saving habits

Setting aside money regularly, even small amounts, becomes routine, helping you grow your savings steadily over time. - You feel more in control

Understanding where your money goes gives you confidence, making it easier to manage your finances and make better decisions.

👉 That’s real progress

Small, consistent improvements lead to lasting financial stability and a stronger sense of control over your money.

Why This Budget Rule Is Perfect for Beginners

Because it:

- Simplifies money decisions

You don’t have to overthink every purchase—just decide which category it belongs to, making budgeting easier and faster to manage. - Reduces overwhelm

With only three categories, you avoid confusion and feel less stressed compared to tracking multiple detailed expenses. - Builds consistent habits

Repeating the same simple structure each month helps you develop strong money habits that become easier to maintain over time.

👉 It gives you a starting point—not pressure

How Budgeting Changes Your Life

This goes beyond money.

Budgeting affects how you think, feel, and make decisions in daily life. It helps you feel more organized, reduces uncertainty, and gives you a clearer sense of direction, making it easier to handle both expected and unexpected financial situations.

1. Less Stress

You know where your money is going.

When you understand your spending, you worry less about unexpected bills or running out of money. Having a clear plan helps you feel prepared, reducing financial anxiety and making daily decisions easier to manage.

2. More Confidence

You start believing:

👉 “I can manage this”

As you follow your budget and see small improvements, you begin to trust your ability to handle money. Making consistent, better decisions builds confidence and encourages you to stay committed to your financial goals.

3. More Freedom

Even small savings give you options.

Having money set aside allows you to handle unexpected situations without panic, make choices more confidently, and avoid relying on debt. Over time, this flexibility gives you greater control over your finances and daily decisions.

4. More Control

You stop reacting—and start planning.

Instead of making last-minute decisions based on urgency, you begin to plan ahead for bills, expenses, and savings. This helps you avoid financial surprises, stay organized, and make choices that support your long-term goals instead of short-term pressure.

Final Thoughts: Keep It Simple

You don’t need a perfect system.

You need a simple one you can follow.

Remember This

👉 Budgeting is not about restriction

👉 It’s about direction

Start Today

- Write your income

- Divide into 3 categories

- Make small adjustments

👉 That’s how real change begins

FAQs

Is the 50/30/20 rule realistic?

Yes—but it may need to be adjusted depending on your income and expenses.

Not everyone can follow the exact percentages right away, especially if income is low or costs are high. The rule is meant to guide your decisions, helping you understand how to balance spending, saving, and financial priorities over time.

Can I use this if I’m broke?

Yes. Start with smaller percentages and build gradually. If your income is limited, focus on covering your needs first, then set aside even a small amount for savings. As your situation improves, you can adjust the percentages and increase what you save over time.

Do I have to follow it exactly?

No. It’s a guideline—not a strict rule. Your income, expenses, and priorities are unique, so your budget should reflect your situation. Adjust the percentages as needed to make your budget realistic and sustainable, while still helping you manage your money effectively.

What if I can’t save 20%?

Start small. Consistency matters more than the amount. If your budget is tight, begin with a small percentage that you can manage comfortably. Saving even a little each month helps you build the habit, and over time, those small amounts can grow into meaningful financial progress.

A Simple, Real-Life Guide to Managing Your Money Without Feeling Overwhelmed

Introduction: Why Budgeting Feels So Confusing

Budgeting sounds simple… until you try to do it.

There are too many methods.

Too many rules.

Too many opinions.

And if you’re just starting, it can feel like:

- “Where do I even begin?”

- “Am I doing this right?”

- “Why does this feel so complicated?”

For many people, budgeting becomes something they avoid—not because they don’t care, but because it feels overwhelming.

That’s where the 50/30/20 budget rule comes in.

It simplifies everything.

Instead of tracking dozens of categories, you divide your money into just three parts.

👉 That’s it.

No complicated systems.

No confusion.

Just a clear starting point that actually works.

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting method that divides your income into three categories:

- 50% → Needs

This portion covers essential living expenses like rent, groceries, transportation, and utilities—costs you must pay to maintain your basic daily life and stability. - 30% → Wants

This includes non-essential spending such as eating out, entertainment, or shopping—things that improve your lifestyle but can be reduced if necessary. - 20% → Savings and Debt

This portion goes toward building your financial future, including saving money, paying off debt, and creating a safety net for unexpected expenses.

Each percentage represents how much of your income should go toward that category, helping you balance living expenses, lifestyle choices, and future financial security.

Why This Budget Rule Works (Especially for Beginners)

Most people don’t fail at budgeting because they’re careless.

They fail because the system is too complicated.

The 50/30/20 rule works because:

- It’s easy to understand

With only three categories, you don’t have to track dozens of expenses, making it simple to follow even if you’re completely new to budgeting. - It’s flexible

You can adjust the percentages based on your income and situation, allowing the method to work whether you’re earning a little or a lot. - It reduces decision fatigue

Instead of constantly wondering if you can afford something, you already know which category it belongs to, making spending decisions quicker and clearer. - It’s realistic for everyday life

It allows room for both essentials and enjoyment, so you can manage your money without feeling restricted or overwhelmed.

Instead of asking:

👉 “Where did my money go?”

You start asking:

👉 “Where should my money go?”

That shift changes everything.

Step 1: Know Your Real Income (Start Here)

Before you can budget anything, you need one number:

👉 Your monthly take-home income

This is the money you actually receive after taxes—not your full salary.

If your paycheck shows $1,200 but you only receive $1,000 after deductions, your budget must be based on the $1,000. Using the correct number helps you avoid overspending, plan accurately, and create a budget that actually works in real life.

What to Include

- Salary or wages

This is your main income from your job, whether paid weekly or monthly, and it forms the foundation of your budget and financial planning. - Side income

Include any extra earnings from small jobs, freelance work, or selling items, even if it varies, so you have a more complete picture of your income. - Any consistent support

Money received regularly from family, government programs, or assistance should be included, since it contributes to what you can actually spend and manage each month.

Why This Matters

If you budget based on money you don’t actually have, your plan will fail.

Using your real income ensures your budget is:

- Accurate

Your numbers reflect what you truly have available, helping you avoid mistakes like overspending or underestimating your expenses. - Sustainable

You can maintain your budget over time because it’s based on realistic income, not expectations that may change or fall short. - Practical

Your budget works in real life, allowing you to pay bills, manage spending, and make decisions without constantly running into financial problems.

Step 2: Break Your Money Into 3 Simple Categories

Now you divide your income into three clear parts.

This is where the 50/30/20 rule becomes powerful.

Instead of tracking every single expense, you group your money into needs, wants, and savings. This makes budgeting easier to understand and manage, helping you quickly see where your money is going and where adjustments may be needed.

1. Needs (50%)

Your Essential Living Expenses

Needs are the expenses you must pay to live and function.

These include the basics required for daily survival, such as housing, food, transportation, and utilities. If these are not paid, your ability to live safely or earn income is affected. Keeping this category within 50% helps you maintain stability while leaving room for other financial priorities.

What Counts as a Need

- Rent or mortgage

This is your housing cost and must be paid consistently to maintain a safe place to live, making it one of your highest financial priorities. - Basic groceries

These are essential food items needed for daily nutrition, and planning simple meals helps keep this expense within your budget. - Transportation

Costs like bus fare or fuel are necessary to get to work or handle daily responsibilities, directly supporting your ability to earn income. - Utilities (electricity, water, phone)

These services keep your home functional and allow you to stay connected, making them essential for both daily living and communication. - Insurance

Payments for health, car, or other coverage protect you from large unexpected expenses, helping prevent financial setbacks during emergencies.

Simple Rule

👉 If you don’t pay it, your life becomes unstable

This helps you quickly identify true needs. Missing rent could lead to losing your home, and skipping utility payments could leave you without electricity or water. Focusing on these essential expenses first ensures your basic living conditions and daily responsibilities are protected.

Beginner Example

- Buying groceries → Need

Groceries provide the basic food you need to eat daily and maintain your health, making them essential for survival and part of your core living expenses. - Ordering fast food → Want

Fast food is convenient but not necessary, and choosing it often increases spending compared to cooking at home, making it a flexible expense you can reduce when needed.

Why This Category Matters

Needs usually take the largest portion of your income.

But here’s the important part:

👉 If your needs go above 50%, your budget becomes tight and stressful.

When most of your money goes toward essentials, there’s little left for savings or unexpected expenses. This can lead to constant pressure, making it harder to manage your finances or improve your situation over time.

Real-Life Scenario

- Monthly income: $1,200

This is your total take-home pay available for all expenses, meaning every dollar must be carefully planned to avoid running short. - Needs should be around: $600

Based on the 50% rule, this is the ideal amount to cover essential living expenses while leaving room for wants and savings. - If your rent alone is $700

Your housing cost already exceeds your needs limit, leaving less money for food, transport, and other essentials.

👉 You already have a problem to solve

This highlights a gap in your budget, showing that adjustments are needed to reduce expenses or increase income.

👉 This doesn’t mean failure—it means awareness

Seeing the issue clearly helps you make better decisions and take steps to improve your financial situation.

2. Wants (30%)

Your Lifestyle and Enjoyment

Wants are expenses that improve your life—but are not essential.

These are things you choose to spend money on for comfort, fun, or convenience. While they’re not required for survival, they help you enjoy your life and stay motivated. Managing this category properly allows you to enjoy spending without losing control of your budget.

What Counts as a Want

- Eating out

Meals from restaurants or fast food are convenient and enjoyable but usually cost more than cooking at home, making them optional rather than essential. - Entertainment

Activities like movies, events, or streaming services are for enjoyment and relaxation, but they are not necessary for daily living. - Subscriptions

Monthly services like streaming platforms or apps add convenience but can often be reduced or canceled if money is tight. - Shopping

Buying clothes, accessories, or non-essential items is based on preference, not necessity, and can be delayed when needed. - Travel

Trips and vacations provide experiences but are not required for daily life, making them flexible and adjustable expenses.

Important Truth

Wants are not bad.

They are part of a balanced life.

Enjoying your money in moderation helps you stay motivated and avoid feeling restricted. When you include reasonable wants in your budget, you’re more likely to stick to it long term instead of giving up or overspending later.

Why This Category Exists

If you remove all wants:

- You feel restricted

Cutting out all enjoyable spending can make your budget feel too strict, leading to frustration and making it harder to stick with over time. - You lose motivation

Without small rewards or enjoyment, budgeting can feel like a constant sacrifice, reducing your willingness to continue managing your money. - You stop budgeting

When a budget feels unrealistic, people often give up completely and return to unplanned spending habits.

This category allows you to enjoy life—without losing control, helping you stay consistent while still making progress financially.

Real-Life Example

- Buying coffee every day

Daily purchases may seem small, but over time they add up and can take a noticeable portion of your monthly budget. - Limit it to a few times per week

Reducing how often you spend allows you to enjoy the same habit while keeping your expenses under control.

👉 You still enjoy it—but within your budget

You don’t have to eliminate what you enjoy, just adjust it so it fits comfortably within your financial plan.

3. Savings and Debt (20%)

Your Future and Financial Growth

This is the most important category for long-term stability.

It focuses on building financial security over time by saving money and reducing debt. While it may not feel urgent, consistently setting money aside helps you prepare for emergencies, avoid future stress, and create a more stable and secure financial situation.

What Goes Here

- Emergency savings

Money set aside for unexpected situations like medical expenses, repairs, or urgent bills, helping you handle problems without relying on debt or falling behind financially. - Debt repayment

Payments toward loans or credit cards reduce what you owe over time, helping you avoid high interest and improve your overall financial position. - Investments

Money used to grow your wealth over time, such as savings accounts or long-term plans, helping you build financial security for the future.

Why This Matters

Without savings:

👉 Every unexpected expense becomes a problem

Even small issues like a repair or medical cost can force you to borrow money or delay important bills, creating added stress and financial pressure.

Without debt repayment:

👉 You stay stuck financially

Ongoing interest and unpaid balances keep increasing what you owe, making it harder to move forward or build any meaningful financial progress over time.

Beginner Tip

If 20% feels impossible:

👉 Start smaller

Begin with an amount you can manage consistently, even if it feels small, so you build the habit without overwhelming your budget.

Even:

- 5%

Setting aside a small portion of your income helps you start saving while still covering your essential expenses. - 10%

A slightly higher amount can speed up your progress, helping you build savings or reduce debt more effectively over time.

👉 Still moves you forward

Any amount saved or used to reduce debt creates progress, making your financial situation more stable step by step.

Step 3: Apply the 50/30/20 Rule (Simple Example)

Let’s make this practical.

Start by taking your monthly income and dividing it into the three categories—needs, wants, and savings. This helps you clearly see how much you can spend in each area, making your budget easier to follow and adjust based on your real financial situation.

Example Budget

Monthly income: $1,000

- Needs → $500

- Wants → $300

- Savings → $200

What This Does

You now have:

- A clear plan

You know exactly how your money should be divided, making it easier to manage your income without confusion or uncertainty. - Defined limits

Each category has a set amount, helping you control spending and avoid going over budget in any area. - Less stress

Having a structured plan reduces financial anxiety because you understand where your money is going and what to expect.

👉 No more guessing

You make decisions based on a clear system, not assumptions, giving you more confidence and control over your finances.

What If Your Budget Doesn’t Fit the 50/30/20 Rule?

This is very common—especially for beginners.

Your income, expenses, or financial situation may not match the ideal percentages right away. That’s normal. The goal is not to fit perfectly into the rule, but to use it as a guide to understand where your money is going and where you can improve over time.

Situation 1: Your Needs Are Too High

Example:

Needs = 70–80%

- Housing takes up most of your income

High rent or mortgage payments can consume a large portion of your earnings, leaving little room for other essential expenses. - Basic living costs are higher than expected

Expenses like groceries, utilities, and transportation may cost more than anticipated, especially with rising prices. - Limited flexibility in your budget

With most of your income going toward needs, it becomes difficult to save, handle emergencies, or adjust spending without financial strain.

Why This Happens

- High rent

Housing costs often take up a large portion of your income, especially in expensive areas, leaving less money available for other essential expenses. - Low income

When earnings are limited, even basic needs can consume most of your budget, making it harder to balance spending and save. - Limited flexibility

Fixed expenses like rent and utilities cannot be easily reduced, making it difficult to adjust your budget without changing your income or living situation.

What You Can Do

- Look for ways to reduce expenses

Review your spending and identify areas where you can cut back, such as lowering utility usage or choosing more affordable options for everyday needs. - Adjust spending habits

Small changes, like cooking at home instead of eating out, can free up money and help you better manage your budget. - Increase income (even slightly)

Earning extra money through small jobs or side activities can help cover gaps and make your budget more manageable.

👉 Even small changes help

Situation 2: You Can’t Save 20%

This is normal.

If your income is limited or your expenses are high, setting aside 20% may feel unrealistic at first. Many beginners face this situation, and it doesn’t mean you’re doing anything wrong—it simply reflects your current financial reality and the need to start gradually.

What to Do Instead

- Start with 1–5%

Begin by saving a small portion of your income that feels manageable, so you can build the habit without putting pressure on your budget. - Build gradually

Increase your savings slowly over time as your income improves or expenses decrease, making the process more realistic and sustainable. - Focus on consistency

Saving regularly, even small amounts, helps you build progress and creates a stable financial habit that grows over time.

👉 Progress matters more than perfection

How to Adjust the Rule for Your Reality

The 50/30/20 rule is not strict.

It’s a guideline.

If You’re Living Paycheck to Paycheck

- 70% Needs

A larger portion of your income goes toward essential expenses like rent, food, and transport, reflecting the reality of limited financial flexibility. - 20% Wants

You still allow some room for personal spending, but keep it controlled to avoid overspending and maintain balance. - 10% Savings

Even a small percentage helps you start building financial security, creating a foundation for future stability over time.

If You Have Debt

Try:

- 50% Needs

Keep essential expenses within half of your income so you can cover basics like housing, food, and utilities without overwhelming your budget. - 20% Wants

Limit lifestyle spending to a smaller portion, allowing enjoyment while staying focused on improving your financial situation. - 30% Debt/Savings

Allocate a larger share toward paying off debt or building savings, helping you reduce financial pressure faster and create long-term stability.

👉 Adjust based on your situation—not someone else’s

Common Mistakes Beginners Make

1. Trying to Be Perfect

- A perfect budget doesn’t exist

Your income, expenses, and priorities will change, so expecting everything to be exact every month can lead to frustration and unrealistic expectations. - 👉 A working budget does

Focus on creating a plan you can follow consistently, even if it’s not perfect, because steady progress is what improves your financial situation over time.

2. Ignoring Small Spending

Small purchases feel harmless—but they add up fast.

Daily expenses like snacks, drinks, or small online purchases may seem insignificant, but over time they can take a noticeable portion of your income. Tracking these costs helps you see patterns and make small adjustments that improve your overall budget.

3. Not Tracking Money

If you don’t track it:

👉 You lose control of it

Without tracking your spending, it becomes difficult to understand where your money is going. This can lead to overspending, missed opportunities to save, and financial stress, making it harder to stay within your budget and improve your situation over time.

4. Giving Up Too Soon

Budgeting is a habit—not a quick fix.

Mistakes are part of the process.

It takes time to adjust your spending, learn your patterns, and build consistency. Missing your budget one week or making a mistake doesn’t mean failure—it’s part of learning. Sticking with it over time is what leads to real financial improvement.

How to Make the 50/30/20 Rule Work in Real Life

1. Start Simple

Don’t overcomplicate it.

Focus on dividing your income into the three main categories without worrying about perfect details. Trying to track everything at once can feel overwhelming, so keeping it simple helps you stay consistent and actually follow your budget over time.

2. Track Your Spending Weekly

This helps you stay aware and adjust quickly.

Checking your spending once a week allows you to catch problems early, such as overspending in one category. This makes it easier to correct your habits before the end of the month and stay within your budget.

3. Adjust Monthly

Your situation will change.

Your budget should too.

Expenses, income, and priorities can shift from month to month, so reviewing your budget regularly helps you stay aligned with your current reality. Making small adjustments ensures your budget continues to work effectively instead of becoming outdated or unrealistic.

4. Be Honest With Yourself

Budgeting only works when you’re realistic about your habits.

If you underestimate your spending or ignore certain expenses, your budget won’t reflect reality. Being honest about where your money goes helps you make better decisions, adjust your plan, and create a budget you can actually follow consistently.

Real-Life Scenario (Beginner Friendly)

Let’s say:

You earn $800/month.

Your Budget

- Needs → $480

- Wants → $240

- Savings → $80

What Happens Over Time

- You reduce small expenses

As you become more aware of your spending, you naturally cut back on unnecessary purchases, freeing up money without making drastic lifestyle changes. - You build saving habits

Setting aside money regularly, even small amounts, becomes routine, helping you grow your savings steadily over time. - You feel more in control

Understanding where your money goes gives you confidence, making it easier to manage your finances and make better decisions.

👉 That’s real progress

Small, consistent improvements lead to lasting financial stability and a stronger sense of control over your money.

Why This Budget Rule Is Perfect for Beginners

Because it:

- Simplifies money decisions

You don’t have to overthink every purchase—just decide which category it belongs to, making budgeting easier and faster to manage. - Reduces overwhelm

With only three categories, you avoid confusion and feel less stressed compared to tracking multiple detailed expenses. - Builds consistent habits

Repeating the same simple structure each month helps you develop strong money habits that become easier to maintain over time.

👉 It gives you a starting point—not pressure

How Budgeting Changes Your Life

This goes beyond money.

Budgeting affects how you think, feel, and make decisions in daily life. It helps you feel more organized, reduces uncertainty, and gives you a clearer sense of direction, making it easier to handle both expected and unexpected financial situations.

1. Less Stress

You know where your money is going.

When you understand your spending, you worry less about unexpected bills or running out of money. Having a clear plan helps you feel prepared, reducing financial anxiety and making daily decisions easier to manage.

2. More Confidence

You start believing:

👉 “I can manage this”

As you follow your budget and see small improvements, you begin to trust your ability to handle money. Making consistent, better decisions builds confidence and encourages you to stay committed to your financial goals.

3. More Freedom

Even small savings give you options.

Having money set aside allows you to handle unexpected situations without panic, make choices more confidently, and avoid relying on debt. Over time, this flexibility gives you greater control over your finances and daily decisions.

4. More Control

You stop reacting—and start planning.

Instead of making last-minute decisions based on urgency, you begin to plan ahead for bills, expenses, and savings. This helps you avoid financial surprises, stay organized, and make choices that support your long-term goals instead of short-term pressure.

Final Thoughts: Keep It Simple

You don’t need a perfect system.

You need a simple one you can follow.

Remember This

👉 Budgeting is not about restriction

👉 It’s about direction

Start Today

- Write your income

- Divide into 3 categories

- Make small adjustments

👉 That’s how real change begins

FAQs

Is the 50/30/20 rule realistic?

Yes—but it may need to be adjusted depending on your income and expenses.

Not everyone can follow the exact percentages right away, especially if income is low or costs are high. The rule is meant to guide your decisions, helping you understand how to balance spending, saving, and financial priorities over time.

Can I use this if I’m broke?

Yes. Start with smaller percentages and build gradually. If your income is limited, focus on covering your needs first, then set aside even a small amount for savings. As your situation improves, you can adjust the percentages and increase what you save over time.

Do I have to follow it exactly?

No. It’s a guideline—not a strict rule. Your income, expenses, and priorities are unique, so your budget should reflect your situation. Adjust the percentages as needed to make your budget realistic and sustainable, while still helping you manage your money effectively.

What if I can’t save 20%?

Start small. Consistency matters more than the amount. If your budget is tight, begin with a small percentage that you can manage comfortably. Saving even a little each month helps you build the habit, and over time, those small amounts can grow into meaningful financial progress.

You have invested time learning today. Now take the next step by downloading our free 7 Days To Financial Clarity™ workbook and begin building a stronger financial future.