Choosing an insurance policy can feel overwhelming.

A quick search online reveals hundreds of insurance companies, countless policy options, and a wide range of prices. Every insurer claims to offer excellent coverage, competitive rates, and reliable protection.

For the average consumer, sorting through all of these choices can be confusing.

Many people aren’t sure where to begin.

Some focus entirely on finding the lowest premium.

Others purchase the first policy recommended to them without fully understanding what it covers.

Unfortunately, both approaches can lead to costly mistakes.

The purpose of insurance is to protect you financially when unexpected events occur.

However, that protection is only valuable if the policy actually meets your needs.

A policy that provides too little coverage may leave you exposed to significant financial risk.

A policy with unnecessary coverage may result in paying far more than you need to.

This is why choosing the right insurance policy matters.

The goal isn’t simply to buy insurance.

The goal is to buy the right insurance.

Whether you’re shopping for:

- Health insurance

- Life insurance

- Auto insurance

- Homeowners insurance

- Renters insurance

- Disability insurance

the same basic principles apply.

You need to understand:

- What risks you’re trying to protect against

- How much coverage you need

- What the policy covers

- What the policy excludes

- How much you’re willing to pay

- Whether the insurance company is trustworthy

Many consumers discover too late that they never fully understood their policy.

Often this realization comes when they attempt to file a claim.

By then, changing the decision may no longer be possible.

The good news is that choosing insurance doesn’t have to be complicated.

Once you understand a few key concepts, evaluating policies becomes much easier.

Throughout this article, you’ll learn:

- How insurance works

- How to evaluate your coverage needs

- What details matter most when comparing policies

- Common mistakes people make

- Warning signs to watch for

- Practical steps for choosing coverage confidently

By the end, you’ll have a framework you can use to evaluate almost any type of insurance policy.

Before discussing how to choose a policy, it’s important to understand why the decision matters in the first place.

Why Choosing the Right Insurance Policy Matters

Many people view insurance as a required expense rather than a financial protection tool.

As a result, they often focus only on price.

While affordability is important, cost should never be the only consideration.

Insurance exists to help protect you from financial loss.

The wrong policy can leave major gaps in that protection.

The right policy can provide valuable security and peace of mind.

Financial Protection vs Financial Waste

Every insurance policy represents a balance.

You want enough coverage to protect yourself from meaningful financial risks without paying for unnecessary benefits.

Finding that balance is one of the most important parts of choosing insurance.

Too Little Protection

If coverage is insufficient, you may face significant out-of-pocket expenses when a claim occurs.

Too Much Protection

If coverage exceeds your actual needs, you may spend money unnecessarily for years.

Neither extreme is ideal.

The goal is appropriate protection.

The Cost of Being Underinsured

Being underinsured means your coverage is insufficient to fully protect you against a potential loss.

This can create serious financial consequences.

Example: Homeowners Insurance

Imagine your home would cost:

$300,000

to rebuild after a disaster.

However, your policy only provides:

$180,000

in coverage.

You may be responsible for covering the remaining difference yourself.

That shortfall could create enormous financial strain.

Example: Life Insurance

Suppose a parent purchases a small life insurance policy that covers only final expenses.

If the family relies on that person’s income, the surviving household may still struggle financially despite receiving the death benefit.

Coverage should be based on actual financial needs rather than arbitrary numbers.

The Cost of Being Overinsured

Although underinsurance receives more attention, overinsurance can also be costly.

Overinsurance occurs when someone purchases significantly more coverage than necessary.

This may result in:

- Higher premiums

- Reduced savings opportunities

- Less efficient use of financial resources

For example, purchasing coverage far beyond realistic financial needs may provide little additional benefit while increasing costs substantially.

The objective is not maximum coverage.

The objective is appropriate coverage.

Real-Life Example

Consider two homeowners.

Homeowner A

Chooses the cheapest available policy without reviewing coverage details.

The policy contains:

- Lower coverage limits

- Higher deductibles

- Significant exclusions

When damage occurs, the homeowner discovers the policy provides less protection than expected.

Homeowner B

Spends time comparing options.

The homeowner reviews:

- Coverage limits

- Deductibles

- Exclusions

- Insurer reputation

Although the premium is slightly higher, the policy provides better protection and fewer surprises.

The Lesson

Insurance decisions should focus on value rather than price alone.

A slightly higher premium may provide substantially better protection.

Understanding this principle is the foundation of smart insurance shopping.

Understanding the Purpose of Insurance

Before evaluating specific policies, it’s helpful to understand what insurance is actually designed to do.

Many consumers assume insurance exists to eliminate risk.

In reality, insurance does something slightly different.

Insurance helps transfer financial risk.

Rather than bearing the entire cost of a potential loss yourself, you share that risk with an insurance company.

This concept applies to nearly every type of insurance.

Insurance Is Risk Management

Life is filled with uncertainty.

Most people cannot predict:

- Accidents

- Illnesses

- Property damage

- Disabilities

- Premature death

These events may be unlikely, but they can be financially devastating.

Insurance helps manage that uncertainty.

Instead of facing potentially catastrophic losses alone, policyholders pay premiums in exchange for financial protection.

Think of insurance as a safety net.

You hope you never need it.

But if something goes wrong, you’ll be glad it’s there.

Protecting Against Financial Loss

Insurance is not primarily about preventing bad things from happening.

Insurance cannot:

- Prevent a car accident

- Stop a house fire

- Eliminate illness

- Prevent death

What insurance can do is reduce the financial consequences of those events.

This distinction is important.

The value of insurance is measured not by whether something happens, but by how effectively it protects you if something does happen.

Common Types of Insurance

Different insurance policies protect against different types of risks.

Understanding the purpose of each can help you determine which types of coverage may be relevant.

Health Insurance

Health insurance helps pay for covered medical expenses.

It can reduce the financial impact of:

- Doctor visits

- Hospital stays

- Emergency care

- Prescription medications

Health insurance is often one of the most important forms of financial protection because healthcare costs can be substantial.

Life Insurance

Life insurance provides a financial benefit to beneficiaries after the insured person’s death.

Its primary purpose is income replacement and financial protection for loved ones.

This type of coverage is often important for:

- Parents

- Married couples

- Homeowners

- Individuals with financial dependents

Auto Insurance

Auto insurance helps protect against financial losses related to vehicle ownership and operation.

Coverage may include:

- Property damage

- Liability protection

- Collision coverage

- Comprehensive coverage

In many locations, certain forms of auto insurance are legally required.

Homeowners Insurance

Homeowners insurance helps protect one of the largest investments many people will ever make.

Coverage may include:

- Property damage

- Personal belongings

- Liability protection

- Additional living expenses

The exact coverage depends on the policy.

Renters Insurance

Many renters assume their landlord’s insurance protects their belongings.

In most cases, it does not.

Renters insurance can help protect:

- Personal possessions

- Liability exposures

- Temporary living expenses after covered losses

Disability Insurance

Disability insurance protects your income if illness or injury prevents you from working.

Because your ability to earn income is often your most valuable financial asset, disability coverage can play an important role in financial planning.

A Key Principle Before Moving Forward

Every insurance decision should begin with a simple question:

What financial risk am I trying to protect against?

People often shop for insurance by looking at premiums first.

However, the smarter approach is identifying risks before comparing policies.

Once you understand the risk, evaluating coverage becomes much easier.

In the next section, we’ll begin the practical process of choosing insurance by identifying the specific risks you need to protect against and determining how those risks relate to your personal financial situation.

==============================================

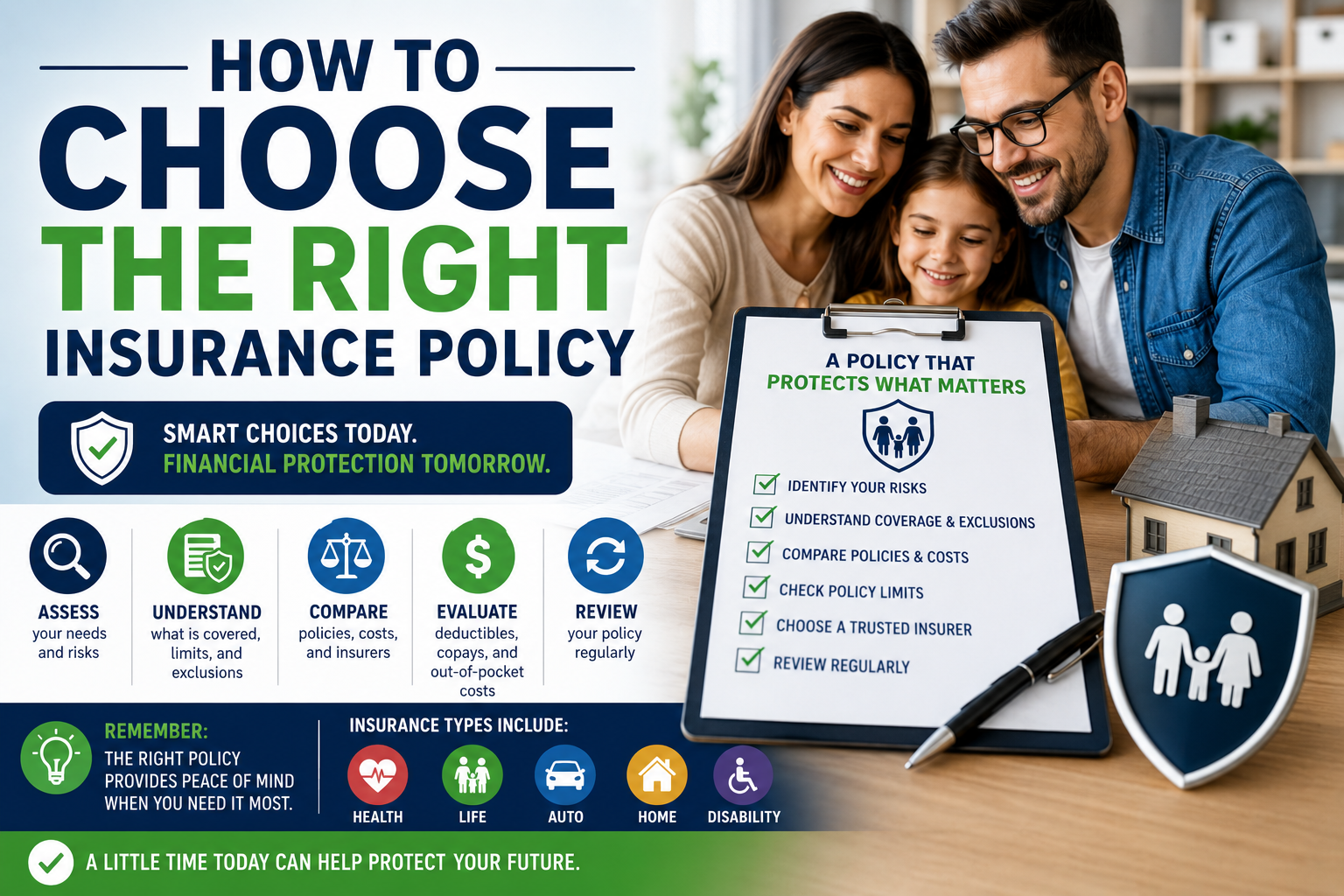

Step 1: Identify What Risks You Need to Protect Against

One of the biggest mistakes people make when shopping for insurance is comparing policies before understanding what they are trying to protect.

Insurance should never be purchased simply because someone recommends it or because a policy appears affordable.

The first step is identifying the specific financial risks that could negatively affect your life, family, or finances.

Once you understand your risks, choosing appropriate coverage becomes much easier.

Think of insurance as a tool.

Just as you would select different tools for different jobs, you should select different insurance policies for different risks.

A homeowner faces different risks than a renter.

A parent faces different risks than a single adult.

A business owner faces different risks than an employee.

Your insurance needs should reflect your personal circumstances.

Assess Your Financial Situation

Your financial situation plays a major role in determining which insurance policies are important and how much coverage you may need.

Start by examining:

- Income

- Savings

- Investments

- Debt obligations

- Monthly expenses

The stronger your financial position, the more flexibility you may have when choosing insurance options.

However, even financially stable individuals can benefit from insurance because certain losses may be too large to absorb comfortably.

Questions to Ask Yourself

Consider:

- Could I pay a large hospital bill without financial hardship?

- Could I rebuild my home after a disaster?

- Could my family maintain their lifestyle if my income disappeared?

- Could I replace a totaled vehicle without assistance?

Your answers help identify areas where insurance may provide valuable protection.

Why This Matters

Insurance is most valuable when it protects against losses that would be financially difficult to handle on your own.

Small expenses can often be managed through savings.

Large, unexpected expenses are where insurance becomes especially important.

Consider Your Family Responsibilities

Insurance needs often increase as family responsibilities grow.

A single adult with no dependents typically has different coverage needs than someone supporting a spouse and children.

Financial Dependents

Ask yourself:

- Does anyone rely on my income?

- Would someone face financial hardship if I died?

- Am I responsible for supporting children?

- Do I help support aging parents?

The more people who depend on you financially, the more important certain types of insurance become.

Real-Life Example

Imagine two individuals:

Sarah

- Single

- No children

- No dependents

Michael

- Married

- Two children

- Primary household income earner

Michael’s need for life insurance is generally much greater because more people depend on his financial support.

The same principle applies to other forms of insurance.

Family responsibilities often increase the consequences of financial loss.

Evaluate Your Assets

Assets represent things you own that have financial value.

Examples include:

- A home

- Vehicles

- Savings accounts

- Investment accounts

- Valuable personal property

- Business interests

The more assets you own, the more important it becomes to protect them.

Protecting What You’ve Built

Many people spend decades building wealth.

A major uninsured loss can undo years of financial progress.

For example:

A homeowner who lacks adequate insurance could face enormous rebuilding costs after a disaster.

Similarly, an individual with substantial assets may need higher liability coverage to help protect against lawsuits and legal claims.

Understanding Asset Protection

Insurance is not just about replacing property.

It’s also about preserving financial stability.

When evaluating policies, consider both:

- The value of your assets

- The potential financial risks those assets face

Think About Worst-Case Scenarios

Although nobody enjoys thinking about disasters or emergencies, this exercise is extremely useful when choosing insurance.

Insurance exists because unexpected events occur.

Ask yourself:

What Happens If…

- I become seriously ill?

- My home is damaged by a fire?

- My vehicle is involved in a major accident?

- I become unable to work?

- I die unexpectedly?

These questions help identify risks that may require financial protection.

Why Worst-Case Thinking Helps

Many people focus only on what is likely to happen.

Insurance planning often requires considering what is possible.

Some events are unlikely but financially devastating.

For example:

A house fire may be rare.

However, the financial consequences could be enormous.

Insurance helps protect against these high-impact risks.

Balancing Probability and Consequences

Not every risk requires insurance.

Generally, insurance is most useful when:

- The financial loss could be significant.

- The event is difficult to predict.

- The consequences would be difficult to absorb personally.

This principle helps explain why insurance is commonly used for major risks rather than minor expenses.

Real-Life Example

Let’s look at how risk assessment works in practice.

Meet David

David is 38 years old.

He is married and has two children.

He owns:

- A home

- Two vehicles

- Retirement savings

- A growing investment account

He is also the primary income earner in his household.

Identifying David’s Risks

David considers several potential risks:

Risk #1: Premature Death

His family depends heavily on his income.

Life insurance becomes an important consideration.

Risk #2: Serious Illness

Medical treatment could be expensive.

Health insurance helps reduce that risk.

Risk #3: Home Damage

His home is one of his largest financial assets.

Homeowners insurance helps protect that investment.

Risk #4: Vehicle Accident

A major accident could create property damage and liability costs.

Auto insurance helps manage that exposure.

The Result

Instead of buying insurance randomly, David identifies specific risks and matches insurance solutions to those risks.

This approach typically results in better protection and more efficient use of financial resources.

Step 2: Determine How Much Coverage You Need

Once you’ve identified the risks you want to protect against, the next question becomes:

How much insurance is enough?

This is where many consumers struggle.

Some purchase the minimum amount available.

Others assume more coverage is always better.

Neither approach is necessarily correct.

The ideal amount of coverage depends on your financial situation, responsibilities, and risk exposure.

The goal is to choose coverage that adequately protects you without paying for unnecessary protection.

Why Coverage Amount Matters

The amount of coverage you purchase directly affects how much financial protection you receive.

A policy that provides insufficient coverage may leave you responsible for substantial expenses.

A policy that provides excessive coverage may result in unnecessarily high premiums.

Finding the right balance is critical.

Example

Suppose a homeowner’s policy provides:

$150,000

of dwelling coverage.

However, rebuilding the home would cost:

$300,000

The policy may not fully protect the homeowner after a major loss.

The issue isn’t whether insurance exists.

The issue is whether enough insurance exists.

The Danger of Too Little Coverage

Underinsurance is one of the most common insurance mistakes.

People often reduce coverage to lower premiums.

Unfortunately, this can create significant financial risks.

Potential Consequences

Insufficient coverage may result in:

- Large out-of-pocket expenses

- Asset depletion

- Increased debt

- Delayed financial recovery

A policy should be designed to provide meaningful protection, not simply satisfy a requirement.

Real-Life Example

A family purchases life insurance equal to one year’s income because it appears affordable.

However, the surviving family would require many years of financial support.

The coverage amount may not adequately meet the family’s needs.

The Cost of Too Much Coverage

While underinsurance receives most of the attention, over-insurance can also create problems.

Excessive coverage often results in:

- Higher premiums

- Reduced investment opportunities

- Less efficient use of financial resources

The objective is not maximum coverage.

The objective is appropriate coverage.

Practical Perspective

Insurance should be based on realistic needs rather than fear.

Coverage should reflect:

- Financial responsibilities

- Asset values

- Income replacement needs

- Potential liabilities

This approach helps create a balanced insurance strategy.

A Simple Coverage Planning Rule

Before purchasing any insurance policy, ask:

What financial loss am I trying to protect against?

Then ask:

How much would that loss realistically cost?

The answer provides a useful starting point for determining coverage needs.

Many insurance decisions become much easier when viewed through this lens.

In the next section, we’ll examine how to evaluate policy details, understand what coverage actually includes, and identify important exclusions that many consumers overlook before purchasing insurance.

==================================================

Step 3: Understand What the Policy Covers

Once you’ve identified the risks you want to protect against and determined how much coverage you may need, the next step is understanding exactly what a policy covers.

This is where many insurance buyers make costly mistakes.

Some consumers assume coverage exists without verifying the details.

Others rely solely on marketing materials or verbal explanations.

Unfortunately, misunderstandings often become apparent only when a claim is filed.

At that point, it may be too late to make changes.

The purpose of reviewing policy coverage is simple:

You need to know exactly what protection you are purchasing.

The more clearly you understand your coverage before buying, the fewer surprises you’re likely to encounter later.

Covered Events

Every insurance policy is designed to protect against specific events.

These events are often called covered perils, covered losses, or covered risks.

The exact terminology varies by policy type.

Examples of Covered Events

Health Insurance

May cover:

- Doctor visits

- Hospital stays

- Emergency care

- Prescription medications

- Preventive services

Auto Insurance

May cover:

- Vehicle collisions

- Theft

- Vandalism

- Weather damage

- Liability claims

Homeowners Insurance

May cover:

- Fire damage

- Wind damage

- Theft

- Certain water-related losses

- Liability incidents

Life Insurance

May provide a death benefit if the insured person dies while the policy remains active.

The key point is that insurance policies only cover specified risks.

Never assume coverage exists simply because a loss seems reasonable.

Always verify it.

Covered Expenses

In addition to understanding covered events, it’s important to understand which expenses are eligible for reimbursement or payment.

Many consumers mistakenly assume all expenses related to a covered event will automatically be paid.

This is not always the case.

Example: Auto Insurance

Suppose your vehicle is involved in an accident.

Your policy may cover:

- Vehicle repairs

- Medical expenses

- Liability claims

However, certain costs may remain your responsibility depending on:

- Deductibles

- Coverage limits

- Policy exclusions

Example: Health Insurance

A medical procedure may be covered.

However, you may still owe:

- Deductibles

- Copays

- Coinsurance

Coverage does not necessarily mean zero cost.

Understanding the difference helps prevent unrealistic expectations.

Policy Limits

Every insurance policy contains limits.

A policy limit is the maximum amount the insurance company will pay under specified circumstances.

Policy limits play a major role in determining the quality of your protection.

Why Limits Matter

Imagine a homeowners policy provides:

$200,000

of dwelling coverage.

If rebuilding your home would cost:

$350,000

you may be responsible for the difference.

The policy exists.

Coverage exists.

But the limit may not be sufficient.

Different Types of Limits

Depending on the policy, limits may apply to:

- Individual claims

- Specific property categories

- Liability coverage

- Lifetime benefits

- Annual benefits

Reviewing limits carefully is one of the most important parts of policy evaluation.

Deductibles

A deductible is the amount you generally pay before insurance begins covering eligible losses.

Deductibles help reduce insurer risk and influence premium costs.

Lower Deductibles

Typically result in:

- Higher premiums

- Lower out-of-pocket costs during claims

Higher Deductibles

Typically result in:

- Lower premiums

- Higher out-of-pocket costs during claims

Neither option is universally better.

The right choice depends on your financial situation.

Example

Suppose you have two homeowners insurance options:

Policy A

Premium:

$1,500 per year

Deductible:

$500

Policy B

Premium:

$1,100 per year

Deductible:

$2,500

Policy B costs less annually but requires greater financial responsibility if a claim occurs.

Understanding this trade-off helps you choose coverage that aligns with your budget and risk tolerance.

Waiting Periods

Some insurance policies contain waiting periods before certain benefits become available.

This is particularly common in:

- Disability insurance

- Health insurance

- Long-term care insurance

Why Waiting Periods Exist

Insurance companies use waiting periods to reduce fraud and discourage individuals from purchasing coverage only after a loss becomes imminent.

Example

A disability insurance policy may include:

90-day waiting period

This means benefits begin only after the waiting period has been satisfied.

Failing to understand waiting periods can create unrealistic expectations about when benefits become available.

Why Reading the Policy Matters

Many people purchase insurance based solely on:

- Advertisements

- Recommendations

- Premium comparisons

While these factors may be helpful, they should never replace reviewing policy details.

Insurance contracts contain important information about:

- Coverage

- Limits

- Deductibles

- Exclusions

- Claims procedures

Ignoring these details increases the likelihood of unpleasant surprises.

A Better Approach

Before purchasing any policy:

✓ Review the summary of coverage.

✓ Review policy limits.

✓ Understand deductibles.

✓ Understand exclusions.

✓ Ask questions about unclear terms.

Taking these steps can significantly improve your insurance decisions.

Step 4: Understand What the Policy Does NOT Cover

Many consumers focus entirely on what a policy covers.

However, understanding what a policy excludes is equally important.

Exclusions are one of the most overlooked aspects of insurance shopping.

Yet they often become critically important during the claims process.

An exclusion identifies situations, losses, or circumstances that are not covered by the policy.

If a claim falls within an exclusion, the insurance company may deny coverage.

Understanding exclusions helps prevent misunderstandings and allows you to make informed decisions.

Exclusions Explained

Every insurance policy contains exclusions.

This does not necessarily mean the policy is bad.

Exclusions are simply part of how insurance works.

Insurance companies define:

- Covered risks

- Non-covered risks

This allows them to manage costs and price policies appropriately.

Why Exclusions Exist

Without exclusions, insurance would become significantly more expensive.

Exclusions help insurers:

- Control risk exposure

- Limit abuse

- Price policies accurately

The goal is to clearly define what is and is not covered.

Common Insurance Exclusions

Although exclusions vary by policy type, several common examples appear frequently.

Health Insurance Exclusions

May include:

- Certain cosmetic procedures

- Experimental treatments

- Non-covered therapies

Auto Insurance Exclusions

May include:

- Intentional damage

- Illegal activities

- Commercial use under personal policies

Homeowners Insurance Exclusions

May include:

- Flood damage

- Earthquake damage

- Normal wear and tear

- Maintenance issues

Life Insurance Exclusions

May include certain situations outlined within the policy contract, particularly during early policy periods.

Because exclusions vary by insurer and policy type, reviewing the actual policy language is essential.

Why Exclusions Matter

A policy may appear comprehensive until a loss occurs.

If that loss falls within an exclusion, the expected protection may not exist.

Real-Life Example

Imagine a homeowner purchases insurance believing all water damage is covered.

Later, flooding damages the property.

The homeowner discovers the policy excludes flood-related losses.

As a result, significant repair costs become the homeowner’s responsibility.

The issue isn’t that insurance failed.

The issue is that the policy never covered flood damage in the first place.

The Lesson

Understanding exclusions before purchasing a policy is far easier than discovering them after a claim occurs.

This is one reason careful policy review is so important.

A Simple Rule for Evaluating Coverage

Whenever you’re reviewing an insurance policy, ask two questions:

What Does This Policy Cover?

and

What Does This Policy Exclude?

Many consumers ask only the first question.

The most informed buyers ask both.

The answers provide a much clearer picture of the protection being offered.

Now that you understand how to evaluate coverage and exclusions, the next step is comparing insurance companies and learning how to distinguish quality insurers from those that may create problems when claims arise.

================================================================

Step 5: Compare Insurance Companies

Once you’ve determined the type of coverage you need and understand what a policy covers, the next step is evaluating the insurance company itself.

Many consumers spend hours comparing premiums but very little time researching the insurer behind the policy.

This can be a costly mistake.

Insurance is a promise.

The policy only has value if the company can fulfill that promise when a claim occurs.

A low premium may look attractive today, but if the company provides poor customer service, delays claims, or creates unnecessary complications during the claims process, the savings may not feel worthwhile later.

Choosing the right insurance company is just as important as choosing the right policy.

Financial Strength

One of the first things to consider is the financial stability of the insurance company.

Insurance companies collect premiums today and may not pay claims until years or even decades later.

Because of this, financial strength matters.

A financially strong insurer is generally better positioned to:

- Pay claims promptly

- Handle large-scale disasters

- Remain stable during economic downturns

- Meet long-term obligations

Why Financial Stability Matters

Imagine purchasing a 30-year life insurance policy.

You want confidence that the insurer will still be financially healthy decades from now.

Similarly, homeowners and auto insurance customers want reassurance that claims can be paid even after widespread disasters.

What to Look For

Although most consumers don’t need to become financial analysts, it can be helpful to review:

- Company history

- Industry reputation

- Independent financial ratings

- Market presence

Larger companies are not automatically better, but stability should always be part of your evaluation.

Customer Service Reputation

Good customer service becomes particularly important when problems arise.

Many insurance experiences are routine.

Premiums are paid.

Policies renew.

Everything functions smoothly.

However, customer service becomes critically important when:

- A claim is filed

- Coverage questions arise

- Billing issues occur

- Policy changes are needed

Questions to Consider

Ask yourself:

- Is customer support easy to reach?

- Are representatives knowledgeable?

- Are issues resolved efficiently?

- Does the company communicate clearly?

Insurance is a long-term relationship.

Strong customer service can make that relationship much more positive.

Claims Process

The true test of an insurance company often occurs during the claims process.

A policy may appear excellent on paper.

What matters most is how the company responds when you actually need help.

A Good Claims Experience

A strong claims process typically includes:

- Clear communication

- Reasonable documentation requirements

- Timely decisions

- Fair claim evaluations

- Efficient payment procedures

Why This Matters

Imagine two insurance companies offering similar coverage.

One processes claims quickly and communicates clearly.

The other creates delays and confusion.

The difference in customer experience can be significant.

This is why evaluating claims handling is often more important than comparing small premium differences.

Online Reviews

Online reviews can provide useful insights.

However, they should be interpreted carefully.

People are generally more likely to leave reviews after extremely positive or extremely negative experiences.

This can create a distorted picture.

What to Focus On

Instead of concentrating on isolated complaints, look for recurring patterns.

Examples include:

- Consistent praise for customer service

- Repeated complaints about claim delays

- Frequent billing issues

- Positive experiences during emergencies

Patterns often provide more useful information than individual reviews.

Use Reviews as One Tool

Online reviews should complement your research rather than replace it.

Combine reviews with:

- Policy comparisons

- Company history

- Financial stability assessments

- Recommendations from trusted sources

This provides a more balanced perspective.

Why the Cheapest Company Isn’t Always Best

Insurance shoppers naturally want to save money.

There’s nothing wrong with seeking competitive pricing.

However, the cheapest option isn’t always the best value.

Low Premiums Can Mean Trade-Offs

A lower premium may result from:

- Higher deductibles

- Lower coverage limits

- Narrower provider networks

- More restrictive policy terms

Without careful review, consumers may compare prices without comparing actual value.

Value vs Price

A slightly more expensive policy may provide:

- Better customer support

- Faster claims handling

- Stronger coverage

- Fewer exclusions

This additional value may justify the higher premium.

Real-Life Example

Imagine two homeowners insurance policies.

Policy A

Annual Premium:

$900

Policy B

Annual Premium:

$1,050

At first glance, Policy A appears more attractive.

However, after reviewing the details, Policy B includes:

- Higher coverage limits

- Better replacement cost protection

- Lower deductible

- Stronger claims reputation

The extra $150 per year may provide significantly greater protection.

The goal is not necessarily to find the cheapest policy.

The goal is to find the best value.

Step 6: Compare Costs Properly

Comparing insurance costs can be surprisingly difficult.

Many consumers focus on the premium because it’s the most visible number.

However, premiums tell only part of the story.

A complete cost comparison requires evaluating several factors.

Looking beyond monthly payments often reveals which policy provides better overall value.

A proper insurance policy comparison involves much more than simply reviewing premiums.

Premiums

The premium is the amount you pay to maintain coverage.

This is usually the first number consumers notice.

Why Premiums Matter

Premiums affect:

- Monthly budgets

- Annual expenses

- Long-term affordability

A policy that strains your budget may be difficult to maintain over time.

But Premiums Are Only One Piece

A lower premium doesn’t automatically mean lower overall costs.

Many low-premium policies shift more financial responsibility to the policyholder when claims occur.

This is why additional factors must also be considered.

Deductibles

A deductible is the amount you generally pay before insurance begins covering eligible losses.

Deductibles can dramatically affect your financial responsibility during a claim.

Lower Deductible

Often results in:

- Higher premium

- Lower out-of-pocket costs during claims

Higher Deductible

Often results in:

- Lower premium

- Higher out-of-pocket costs during claims

Example

Suppose two auto insurance policies offer identical coverage.

Policy A

Premium:

$1,200 annually

Deductible:

$500

Policy B

Premium:

$950 annually

Deductible:

$2,000

Policy B saves money upfront but creates greater financial exposure if an accident occurs.

The better option depends on your financial situation and risk tolerance.

Copays

Certain insurance policies, particularly health insurance plans, include copayments.

A copay is a fixed amount you pay for specific services.

Examples may include:

- Doctor visits

- Specialist appointments

- Prescription medications

When comparing health insurance plans, reviewing copays can provide a more accurate picture of expected healthcare costs.

Why Copays Matter

A plan with slightly higher premiums may offer significantly lower copays.

For someone who uses healthcare services frequently, this could reduce overall expenses.

Coinsurance

Coinsurance represents your percentage of healthcare costs after meeting the deductible.

For example:

Insurance pays:

80%

You pay:

20%

Although percentages may seem small, they can become significant during major medical events.

Example

Medical procedure cost:

$20,000

Coinsurance:

20%

Your responsibility:

$4,000

Understanding coinsurance helps prevent surprises when evaluating healthcare plans.

Out-of-Pocket Costs

When comparing insurance policies, consider total potential costs rather than premiums alone.

Potential expenses may include:

- Deductibles

- Copays

- Coinsurance

- Non-covered services

- Policy limitations

This broader perspective provides a more realistic understanding of financial exposure.

Looking at the Full Picture

Imagine two health insurance plans.

Plan A

Monthly Premium:

$250

Deductible:

$5,000

Plan B

Monthly Premium:

$400

Deductible:

$1,000

Someone expecting frequent medical care may spend less overall with Plan B despite the higher premium.

This illustrates why comprehensive comparisons are so important.

Looking Beyond Monthly Payments

One of the most valuable habits insurance shoppers can develop is looking beyond the premium.

A complete evaluation considers:

✓ Coverage limits

✓ Deductibles

✓ Exclusions

✓ Claims reputation

✓ Customer service

✓ Out-of-pocket costs

✓ Financial strength

When viewed together, these factors provide a much clearer picture of a policy’s true value.

A Smarter Way to Compare Insurance

Instead of asking:

“Which policy is cheapest?”

Ask:

“Which policy provides the best protection for the cost?”

This subtle shift often leads to better insurance decisions.

The cheapest policy may save money today.

The best-value policy may save far more when a claim occurs.

In the next section, we’ll explore policy limits, liability protection, replacement cost versus actual cash value, and the critical questions every consumer should ask before signing an insurance contract.

==========================================================

Step 7: Review Your Policy Limits

Many consumers spend considerable time comparing premiums but very little time reviewing policy limits.

This can be a costly oversight.

Policy limits determine the maximum amount an insurance company will pay for a covered loss.

In many ways, policy limits define the true value of an insurance policy.

A policy with excellent pricing means very little if the limits are insufficient to protect you when a major loss occurs.

Understanding policy limits is one of the most important steps in choosing the right insurance coverage.

Coverage Limits Explained

A coverage limit is the maximum amount an insurer will pay for a covered claim.

These limits vary depending on:

- Policy type

- Coverage category

- Insurance company

- Coverage options selected

Many policies contain multiple limits rather than a single overall limit.

Examples

Auto Insurance

May include separate limits for:

- Bodily injury liability

- Property damage liability

- Collision coverage

- Uninsured motorist coverage

Homeowners Insurance

May include limits for:

- Dwelling coverage

- Personal property

- Liability protection

- Additional living expenses

Health Insurance

May include various cost-sharing limits and out-of-pocket maximums.

Understanding these limits helps you determine whether the policy provides adequate protection.

Why Coverage Limits Matter

Insurance exists to help protect against significant financial losses.

If limits are too low, you may still face substantial out-of-pocket expenses after a claim.

Real-Life Example

Imagine your homeowners policy provides:

$250,000

of dwelling coverage.

However, rebuilding your home after a disaster would cost:

$400,000

The insurance company may only pay up to the policy limit.

You could be responsible for the remaining amount.

This illustrates why selecting appropriate limits is so important.

Reviewing Limits Regularly

Coverage needs often change over time.

Factors that may affect policy limits include:

- Rising construction costs

- Inflation

- Increased property values

- New assets

- Changes in family circumstances

A policy that was adequate five years ago may no longer provide sufficient protection today.

Annual reviews help ensure your coverage keeps pace with your changing needs.

Replacement Cost vs Actual Cash Value

When comparing property insurance policies, one of the most important distinctions involves how losses are valued.

Two common approaches are:

- Replacement Cost

- Actual Cash Value

Understanding the difference can significantly affect claim outcomes.

What Is Replacement Cost?

Replacement cost coverage generally helps pay the amount required to replace damaged property with a similar new item.

Depreciation is not deducted.

Example

Suppose your five-year-old television is destroyed during a covered event.

A comparable replacement television costs:

$800

With replacement cost coverage, the insurer may help cover the cost of replacing the television with a similar new model according to policy terms.

Advantages

Replacement cost coverage often provides:

- Better financial protection

- Reduced out-of-pocket expenses

- Easier recovery after losses

Because of these benefits, many consumers prefer replacement cost coverage when available.

What Is Actual Cash Value?

Actual cash value takes depreciation into account.

Instead of paying the cost of a new replacement, the insurer considers the item’s age and condition.

Example

The same television originally cost:

$800

After several years of use, its actual cash value may be determined to be:

$300

Under an actual cash value policy, reimbursement may be based on the depreciated value rather than the replacement cost.

Potential Drawbacks

Policyholders may need to contribute additional money to replace damaged items.

This can create unexpected expenses following a loss.

Which Is Better?

Neither option is universally correct.

However, replacement cost coverage generally provides stronger protection because it better reflects the cost of replacing damaged property in today’s market.

When comparing policies, understanding which valuation method applies is extremely important.

Liability Coverage

Many people focus on protecting their own property while overlooking another major risk:

Liability.

Liability coverage helps protect you when you are legally responsible for causing injury or damage to others.

For many households, liability protection may be one of the most important components of an insurance policy.

Why Liability Coverage Matters

Lawsuits and legal claims can be expensive.

Even relatively minor incidents may result in significant financial exposure.

Examples include:

- Auto accidents

- Injuries on your property

- Property damage caused to others

- Certain personal liability claims

Without adequate liability coverage, personal assets may be at risk.

Real-Life Example

Imagine you are involved in an automobile accident and are found responsible for significant injuries.

Medical expenses and legal claims could potentially exceed tens or hundreds of thousands of dollars.

Adequate liability insurance may help provide financial protection in these situations.

Protecting Assets

Liability coverage can help protect:

- Savings

- Investments

- Property

- Future income

This is one reason financial professionals often recommend reviewing liability limits carefully rather than selecting minimum coverage requirements automatically.

Why Limits Matter

When evaluating insurance policies, many consumers ask:

“What is the premium?”

A better question is:

“What level of protection am I actually receiving?”

Higher limits often provide stronger financial protection.

However, they also generally increase premiums.

The objective is finding the right balance between affordability and risk protection.

A Helpful Perspective

Think of policy limits as the size of your financial safety net.

A larger safety net may cost more, but it may also provide greater protection when you need it most.

Step 8: Ask the Right Questions Before Buying

One of the easiest ways to avoid insurance mistakes is to ask good questions before purchasing a policy.

Many consumers feel uncomfortable asking detailed questions.

However, insurance is a financial product.

Understanding what you’re buying is entirely reasonable.

The more information you gather before purchasing coverage, the better your decisions are likely to be.

What Is Covered?

Start with the most obvious question.

Ask:

- What events are covered?

- What losses qualify for reimbursement?

- What benefits are included?

Never assume coverage exists.

Request clear explanations.

If possible, review written documentation.

What Is Excluded?

This question is just as important.

Ask:

- What situations are not covered?

- Are there important exclusions?

- Are additional endorsements available?

Understanding exclusions often prevents future disappointment.

What Are My Responsibilities?

Insurance policies frequently require policyholders to meet certain obligations.

Examples may include:

- Reporting claims promptly

- Maintaining property

- Paying premiums on time

- Providing documentation

Knowing your responsibilities helps ensure coverage remains effective.

How Are Claims Handled?

A policy’s true value often becomes apparent during a claim.

Ask questions such as:

- How do I file a claim?

- What documentation is required?

- How long does the process typically take?

- How are claim decisions made?

Understanding the claims process beforehand can reduce stress later.

Common Insurance Buying Mistakes

Even intelligent consumers make insurance mistakes.

Understanding these common errors can help you avoid them.

Buying Based Only on Price

This is perhaps the most common mistake.

A low premium may seem attractive.

However, lower prices often involve trade-offs.

Examples include:

- Lower limits

- Higher deductibles

- More exclusions

- Reduced benefits

The cheapest policy isn’t always the best value.

Ignoring Exclusions

Many people focus entirely on covered benefits.

Exclusions often receive little attention until a claim occurs.

Reviewing exclusions before purchasing coverage can prevent unpleasant surprises.

Choosing Insufficient Coverage

Underinsurance remains one of the biggest risks in personal finance.

Consumers sometimes reduce coverage to save money without fully considering potential consequences.

A policy should provide meaningful protection, not simply satisfy a requirement.

Failing to Compare Policies

Some buyers accept the first quote they receive.

Comparing multiple options often reveals important differences involving:

- Coverage

- Pricing

- Deductibles

- Customer service

Comparison shopping is usually worthwhile.

Not Reviewing Policies Regularly

Insurance needs change.

A policy that worked well several years ago may no longer be appropriate today.

Major life events often require coverage reviews.

Examples include:

- Marriage

- Children

- Home purchases

- Career changes

- Retirement

Regular reviews help ensure ongoing protection.

Real-Life Examples

Understanding insurance becomes easier when viewed through practical situations.

Example 1: Choosing Life Insurance

Coverage Comparison

James is a 35-year-old father of two.

He receives two life insurance quotes.

Policy A

- Lower premium

- Smaller death benefit

Policy B

- Slightly higher premium

- Significantly larger death benefit

Better Decision Process

Instead of focusing solely on price, James evaluates:

- Family income needs

- Mortgage obligations

- Future education costs

He selects the policy that better protects his family’s financial future.

Lesson

Coverage should reflect actual financial responsibilities.

Example 2: Choosing Health Insurance

Comparing Deductibles and Premiums

Sarah is deciding between two health insurance plans.

Plan A

- Low premium

- High deductible

Plan B

- Higher premium

- Lower deductible

Because Sarah expects regular medical care, Plan B may result in lower overall healthcare expenses despite the higher premium.

Lesson

Comparing total costs is often more important than comparing premiums alone.

Example 3: Choosing Home Insurance

Understanding Coverage Limits

Michael owns a home valued at substantially more than the limit provided by a basic policy.

Instead of choosing the cheapest option, he evaluates rebuilding costs and upgrades his coverage.

Result

If a major loss occurs, the policy is more likely to provide adequate financial protection.

Lesson

Policy limits should align with actual exposure rather than minimum requirements.

A Simple Insurance Buying Formula

Before purchasing any insurance policy, ask yourself:

- What risk am I protecting against?

- How large could the financial loss be?

- Does the policy provide enough coverage?

- What exclusions exist?

- Is the insurer financially stable?

- Am I comparing value rather than price?

These questions can dramatically improve insurance decisions.

In the final section, we’ll cover how often insurance policies should be reviewed, red flags to watch for, your personal insurance checklist, realistic expectations, FAQs, and final recommendations for choosing coverage with confidence.

How Often Should You Review Your Insurance Policies?

Many people purchase insurance and then rarely think about it again.

Years pass.

Life changes.

Financial circumstances evolve.

Yet the insurance policy remains exactly the same.

This can create significant gaps in protection.

Insurance should not be viewed as a one-time decision.

Instead, it should be reviewed periodically to ensure it continues to match your needs.

A policy that was appropriate five years ago may no longer provide adequate protection today.

Major Life Events

Certain life events should automatically trigger an insurance review.

These events often change your financial responsibilities and risk exposure.

Examples include:

- Getting married

- Having children

- Purchasing a home

- Starting a business

- Changing jobs

- Receiving an inheritance

- Paying off major debts

- Retirement

Each of these milestones can affect the amount and type of coverage you need.

Real-Life Example

Suppose a single individual purchases life insurance.

Several years later, that person gets married and becomes a parent.

The original policy may no longer provide sufficient protection for the family’s financial needs.

A review helps identify these gaps before they become problems.

Annual Reviews

Even if no major life changes occur, reviewing your insurance annually is a smart habit.

An annual review allows you to:

- Verify coverage limits

- Evaluate premiums

- Compare policy options

- Confirm beneficiary information

- Update personal information

Many insurance professionals recommend reviewing coverage at least once per year.

This doesn’t necessarily mean changing policies every year.

It simply means ensuring your coverage still aligns with your circumstances.

Changes in Financial Situation

As your finances improve, your insurance needs may change.

Examples include:

- Increased income

- Growing investments

- Additional property ownership

- New business interests

Similarly, major financial setbacks may require adjustments to maintain affordability while preserving important protection.

Insurance should evolve alongside your financial life.

Insurance Red Flags to Watch For

Not every insurance policy provides the same level of protection.

Likewise, not every insurance company operates with the same standards.

Understanding potential warning signs can help you avoid costly mistakes.

Unrealistically Low Prices

Everyone likes saving money.

However, unusually low premiums deserve closer examination.

A dramatically lower price may indicate:

- Reduced coverage

- Higher deductibles

- More exclusions

- Lower policy limits

The cheapest policy is not automatically a bad policy.

However, it should always be reviewed carefully.

Ask Yourself

Why is this policy significantly cheaper than comparable options?

The answer often reveals important differences.

Confusing Policy Language

Insurance contracts can be complex.

However, companies should still be able to explain coverage clearly.

If:

- Terms seem intentionally vague

- Questions go unanswered

- Coverage details remain unclear

consider it a warning sign.

Consumers should understand what they are purchasing before committing to a policy.

Poor Customer Reviews

No insurance company receives perfect reviews.

However, repeated complaints involving:

- Claim delays

- Communication problems

- Billing disputes

- Coverage misunderstandings

may indicate larger issues.

Look for patterns rather than isolated incidents.

Limited Coverage Details

Be cautious when an insurer focuses heavily on price but provides limited information about:

- Coverage

- Exclusions

- Deductibles

- Policy limits

Transparency is important.

A quality insurer should clearly explain what is being offered.

Creating Your Personal Insurance Checklist

One of the best ways to improve insurance decisions is to use a structured checklist.

This helps ensure important details aren’t overlooked.

Before Buying

✓ Identify the risks you want to protect against

✓ Determine how much coverage you need

✓ Establish a realistic budget

✓ Research multiple insurers

✓ Understand policy terminology

During Comparison Shopping

✓ Compare coverage limits

✓ Compare deductibles

✓ Compare exclusions

✓ Compare customer service reputation

✓ Compare claims processes

✓ Compare overall value rather than price alone

Before Signing

✓ Read the policy summary

✓ Review exclusions carefully

✓ Confirm coverage limits

✓ Verify deductibles

✓ Ask questions about anything unclear

✓ Confirm beneficiary information when applicable

During Annual Reviews

✓ Review major life changes

✓ Update beneficiaries

✓ Evaluate coverage limits

✓ Compare renewal pricing

✓ Consider new insurance needs

Using a checklist helps transform insurance shopping from an emotional decision into a structured financial decision.

Realistic Expectations

Insurance is one of the most valuable financial tools available.

However, it is important to understand what insurance can and cannot do.

Consumers who maintain realistic expectations are generally more satisfied with their coverage.

What Insurance Can Do

Insurance can:

- Reduce financial risk

- Help pay covered losses

- Protect assets

- Provide financial stability

- Improve peace of mind

For many households, insurance acts as a financial safety net that helps prevent major setbacks.

What Insurance Cannot Do

Insurance cannot:

- Prevent accidents

- Prevent illnesses

- Eliminate all financial losses

- Cover every possible situation

- Replace careful financial planning

This distinction is important.

Insurance helps manage risk.

It does not eliminate risk entirely.

Understanding Risk Transfer

At its core, insurance is a risk-transfer tool.

Instead of accepting the full financial burden of a potential loss, you transfer part of that risk to an insurance company.

In exchange, you pay premiums.

The success of this arrangement depends on choosing coverage that aligns with your actual needs.

This is why thoughtful policy selection is so important.

The Cost of Choosing the Wrong Insurance Policy

Choosing the wrong insurance policy can be expensive in ways that are not immediately obvious.

Some people discover too late that their policy limits are too low. Others learn that important losses are excluded from coverage. Some focus entirely on premium costs and overlook deductibles, liability limits, or claim restrictions.

Insurance is most valuable before a loss occurs. Taking the time to evaluate coverage carefully today can help prevent financial surprises tomorrow.

Final Thoughts

Choosing the right insurance policy isn’t about finding the cheapest premium or purchasing the largest amount of coverage available.

It’s about finding the right balance between protection, affordability, and financial responsibility.

Throughout this article, we’ve explored a practical framework for making better insurance decisions.

We’ve discussed:

- Identifying risks

- Evaluating coverage needs

- Understanding policy limits

- Reviewing exclusions

- Comparing insurers

- Assessing costs properly

- Avoiding common mistakes

The most important lesson is that insurance should be purchased intentionally.

Every policy should serve a purpose.

Before buying coverage, ask yourself:

What financial risk am I trying to protect against?

That simple question can eliminate much of the confusion that surrounds insurance shopping.

Remember:

The best insurance policy is not necessarily the cheapest.

It is not necessarily the most expensive.

It is the policy that provides appropriate protection for your specific needs.

Taking the time to compare options, review details, and ask questions can help you make informed decisions that protect your finances for years to come.

Insurance may never be the most exciting financial topic.

But choosing the right coverage can be one of the smartest financial decisions you’ll ever make.

Frequently Asked Questions

How do I know which insurance policy is right for me?

Start by identifying the financial risks you want to protect against. Then evaluate your coverage needs, budget, and personal circumstances. The right policy provides appropriate protection without unnecessary costs.

Should I always choose the cheapest insurance policy?

Not necessarily. Lower-priced policies may include lower coverage limits, higher deductibles, or more exclusions. Comparing overall value is usually more important than comparing premiums alone.

How much insurance coverage do I need?

Coverage needs depend on the type of insurance and your financial situation. Consider the potential cost of a loss and choose coverage that would provide meaningful financial protection.

What are insurance exclusions?

Exclusions are situations, losses, or events that are not covered by an insurance policy. Understanding exclusions is essential because they affect when benefits may or may not be available.

Why do insurance companies have deductibles?

Deductibles help reduce insurer risk and encourage responsible claim usage. Higher deductibles often result in lower premiums, while lower deductibles typically increase premium costs.

How often should I review my insurance policies?

At least once per year and whenever major life changes occur. Regular reviews help ensure your coverage remains aligned with your needs and financial responsibilities.

What questions should I ask before buying insurance?

Ask what is covered, what is excluded, what the policy limits are, how claims are handled, and what responsibilities you have as a policyholder.

What is a policy limit?

A policy limit is the maximum amount an insurance company will pay for a covered loss. Limits vary by policy and coverage type.

What happens if I’m underinsured?

If coverage is insufficient, you may be responsible for significant out-of-pocket expenses after a loss. This can create financial hardship and delay recovery.

Can I switch insurance companies later?

Yes. Many consumers change insurers when better coverage, pricing, or service becomes available. Before switching, review the new policy carefully to ensure there are no gaps in coverage.

What is a policy limit?

Policy limits are important because they determine the maximum financial protection available during a covered claim. Choosing limits that are too low may leave you responsible for significant expenses after a loss.