If you’re new to personal finance, it’s easy to see why secured credit cards and debit cards are often confused.

Both cards can be used to make purchases online and in stores. Both fit in your wallet. Both may require money upfront in some way. When you swipe, tap, or insert either card at a checkout terminal, the process often appears identical.

Because of these similarities, many beginners assume secured credit cards and debit cards are essentially the same thing.

They are not.

Although both cards can help you manage daily spending, they function very differently behind the scenes. Understanding those differences is important because one can help build your credit history while the other generally cannot.

Choosing the wrong tool for your financial goals may slow your progress. Someone trying to build credit may mistakenly rely solely on a debit card and wonder why their credit score never improves. Meanwhile, another person may avoid a secured credit card because they incorrectly believe it works exactly like a prepaid card.

These misunderstandings are common.

The good news is that once you understand how each card works, the differences become much easier to recognize.

In this guide, you’ll learn:

- What debit cards are

- How secured credit cards work

- Why people confuse the two

- Which card helps build credit

- The advantages and disadvantages of each option

- Which card may be better for your situation

- Whether it makes sense to use both together

By the end of this article, you’ll understand exactly how secured credit cards and debit cards differ and how each can fit into a healthy financial strategy.

Let’s begin by looking at the debit card, since it is often the first financial card many people use.

What Is a Debit Card?

A debit card is a payment card linked directly to your checking account or bank account.

When you use a debit card, money is typically withdrawn directly from your available account balance.

In simple terms, you are spending your own money rather than borrowing money from a lender.

Because debit cards are connected to your bank account, they are one of the most common financial tools used for everyday purchases.

Many people receive a debit card automatically when they open a checking account.

How Debit Cards Work

Using a debit card is straightforward.

Suppose your checking account contains $1,000.

If you make a $100 purchase using your debit card, the funds are generally deducted from your account balance.

Your available balance would then decrease to approximately $900.

Unlike credit cards, there is no borrowing involved.

You are simply accessing money you already own.

This makes debit cards easy to understand and manage, particularly for beginners who want to avoid debt.

Spending Your Own Money

One of the biggest advantages of a debit card is that it encourages spending within your available resources.

Because purchases come directly from your bank account, there is often a natural spending limit.

For example:

- Bank account balance: $500

- Purchase amount: $50

New balance: $450

Once the money is gone, additional spending becomes limited unless new funds are deposited.

This structure helps many people avoid overspending.

However, it can also create limitations when trying to establish a credit history.

We’ll discuss that issue later in this guide.

Where Debit Cards Are Accepted

Modern debit cards are accepted at most locations that accept major payment networks.

This includes:

- Grocery stores

- Restaurants

- Online retailers

- Gas stations

- Subscription services

- Utility payments

For everyday spending, debit cards provide convenience similar to credit cards.

From a consumer’s perspective, the checkout experience often feels almost identical.

This similarity is one reason many beginners struggle to distinguish between debit cards and secured credit cards.

Advantages of Debit Cards

Debit cards offer several benefits.

Easy to Use

Most people understand the concept of spending money already available in their account.

This simplicity makes debit cards beginner friendly.

Helps Avoid Debt

Because you are spending your own funds, there is generally less risk of accumulating credit card debt.

Widely Accepted

Debit cards can be used almost anywhere that accepts major payment cards.

Direct Account Access

Purchases are reflected quickly within your bank account, making spending easier to monitor.

While debit cards are useful financial tools, they operate very differently from secured credit cards.

To understand why, let’s examine how secured credit cards actually work.

What Is a Secured Credit Card?

A secured credit card is a type of credit card that requires a refundable security deposit.

The deposit serves as collateral for the lender and reduces the lender’s risk when extending credit.

Although the deposit requirement causes confusion, secured credit cards are still genuine credit cards.

They are not prepaid cards.

They are not debit cards.

They are credit products designed to help people establish or rebuild credit histories.

How Secured Credit Cards Work

When opening a secured credit card account, you provide a cash deposit.

For example:

- Deposit $200

- Credit limit approximately $200

or

- Deposit $500

- Credit limit approximately $500

After the account is opened, you can begin using the card for purchases.

Importantly, you are not directly spending your deposit.

Instead, you are borrowing against a credit line provided by the lender.

At the end of each billing cycle, you receive a statement and are expected to make payments.

This process is very different from how debit cards operate.

Why Security Deposits Cause Confusion

Many beginners see the deposit requirement and assume secured credit cards function exactly like debit cards.

This misunderstanding is understandable.

Both involve money provided upfront.

However, the purpose of that money is different.

With a debit card:

- The money remains available for spending.

With a secured card:

- The deposit serves as collateral.

The lender holds the deposit while extending a line of credit.

Your purchases are not automatically deducted from the deposit.

Instead, you receive a bill and repay borrowed funds.

This distinction is extremely important.

Borrowing vs Spending Your Own Money

This is perhaps the most important difference in the entire article.

When you use a debit card:

You spend your own money.

When you use a secured credit card:

You borrow money from a lender and repay it later.

Although the purchase process looks similar, the financial mechanics are fundamentally different.

Credit Reporting Basics

Another major difference involves credit reporting.

Most secured credit cards report account activity to major credit bureaus.

This reporting may include:

- Payment history

- Account balances

- Credit utilization

- Account status

This information can help establish a credit profile.

Debit cards generally do not report spending activity to credit bureaus.

As a result, they typically do not contribute directly to credit-building efforts.

Understanding this difference is the foundation for understanding why secured credit cards exist and why many people use them to establish credit.

Why People Confuse Secured Credit Cards and Debit Cards

If secured credit cards and debit cards work so differently, why do so many people confuse them?

The answer is simple.

On the surface, they appear remarkably similar.

Both are plastic payment cards.

Both can be used at stores and online.

Both may involve money that you already have available.

Without understanding what happens behind the scenes, the differences are not immediately obvious.

Both Require Money Up Front

With a debit card, you need money in your bank account.

With a secured credit card, you need money for the security deposit.

Because both require access to cash, many people assume they function the same way.

The reality is that the money serves entirely different purposes.

Similar Appearance

Most debit cards and secured credit cards look almost identical.

They contain:

- Card numbers

- Expiration dates

- Security codes

- Payment network logos

At a glance, there may be no obvious indication of how the card functions.

Similar Checkout Experience

Whether you swipe, insert, or tap the card, the purchasing process often looks exactly the same.

The payment terminal does not explain whether funds are coming from a bank account or a credit line.

This contributes significantly to consumer confusion.

The Critical Difference Most People Miss

The most important distinction is what happens after the purchase.

With a debit card:

The money leaves your bank account.

With a secured credit card:

The balance is added to your credit account and must be repaid later.

That single difference changes everything from credit-building potential to borrowing behavior.

Now that we’ve clarified why these cards are frequently confused, let’s examine the biggest distinction between them in greater detail.

The Biggest Difference: Borrowing vs Spending

If you remember only one concept from this entire article, make it this one:

A debit card spends your money. A secured credit card borrows money.

This difference affects everything from how purchases are processed to whether your activity can help build credit.

Although both cards may look the same in your wallet, they serve fundamentally different purposes.

Understanding this distinction can help you choose the right financial tool for your goals.

Debit Cards Use Your Bank Account Balance

When you use a debit card, the money comes directly from your checking account.

Suppose you have:

- Account balance: $1,000

You make a purchase for:

- $100

Your account balance becomes approximately:

- $900

The transaction uses money you already own.

There is no borrowing involved.

Because of this, debit cards are often viewed as spending tools rather than credit-building tools.

They provide convenient access to your own funds without creating debt.

Secured Credit Cards Use a Credit Line

A secured credit card works differently.

Even though you provided a security deposit when opening the account, purchases are generally made using a credit line provided by the lender.

For example:

- Security deposit: $300

- Credit limit: $300

If you spend $100, the lender temporarily covers that purchase.

Your balance increases by $100, and you are expected to repay that amount according to the card agreement.

The transaction is considered borrowing, not spending your own deposit.

This is why secured credit cards are classified as credit products.

Why This Difference Matters

The distinction between spending and borrowing has significant financial implications.

When you borrow money and repay it responsibly, lenders gain information about your financial behavior.

This information may be reported to credit bureaus.

When you simply spend money from your own bank account, there is usually no borrowing activity to report.

As a result:

- Debit cards help manage spending.

- Secured credit cards help build credit.

Understanding this difference is essential when deciding which card better supports your financial goals.

This naturally leads to one of the most common questions beginners ask:

Can a debit card help build credit?

Can a Debit Card Build Credit?

Many people assume that because they use their debit card regularly, their activity should help improve their credit score.

This assumption seems logical.

After all, responsible money management demonstrates financial discipline.

However, credit scores are designed to measure how borrowers manage borrowed money.

Because debit cards do not involve borrowing, they generally do not contribute directly to credit-building.

Why Debit Cards Usually Do Not Report to Credit Bureaus

Most debit card transactions are not reported to major credit bureaus.

When you purchase groceries, fuel, or clothing with a debit card, you are simply accessing your own funds.

Since no credit is being extended, there is typically no borrowing activity for credit bureaus to track.

As a result:

- Purchases are not reported.

- Payments are not reported.

- Spending behavior does not appear on traditional credit reports.

This is one of the primary reasons debit cards do not usually help build credit.

Common Misunderstandings About Banking Activity

Many consumers believe that maintaining a healthy checking account automatically improves credit scores.

While responsible banking habits are beneficial, they generally operate separately from traditional credit reporting systems.

For example:

You may:

- Keep thousands of dollars in savings.

- Never overdraw your account.

- Use your debit card responsibly for years.

Despite these positive behaviors, your credit score may remain unchanged if you have no credit accounts.

This often surprises people who are new to personal finance.

What Actually Builds Credit?

Credit-building activities generally involve borrowed money.

Examples include:

- Credit cards

- Auto loans

- Student loans

- Mortgages

- Certain personal loans

Lenders report repayment behavior to credit bureaus, creating a record of how you manage credit obligations.

This record forms the basis of your credit profile.

Without borrowing activity, there is often little information available to generate a traditional credit score.

This is where secured credit cards can become valuable.

Unlike debit cards, secured cards often provide direct opportunities to establish credit history.

Can a Secured Credit Card Build Credit?

In many cases, yes.

Helping people establish or rebuild credit is one of the primary reasons secured credit cards exist.

For individuals with little or no credit history, secured cards often provide one of the most accessible pathways into the credit system.

Reporting to Credit Bureaus

Most reputable secured credit card issuers report account activity to major credit bureaus.

This reporting may include:

- Payment history

- Current balances

- Credit limits

- Account age

- Account status

Because this information appears on credit reports, responsible card usage may contribute positively to your credit profile.

This is one of the biggest differences between secured credit cards and debit cards.

Payment History Benefits

Payment history is often among the most important factors in credit scoring models.

Every time you make a payment on time, you create a record of responsible borrowing behavior.

Imagine two secured card users:

User A

- Pays every bill on time

- Maintains low balances

- Uses the card regularly

User B

- Frequently pays late

- Misses due dates

- Carries excessive balances

Although both have secured cards, User A is likely to experience better credit-building results.

The card itself is not responsible for the improvement.

Responsible behavior is.

Credit Utilization Benefits

Credit utilization measures how much available credit you are using.

Lower utilization rates generally signal responsible credit management.

Example:

Credit Limit

$500

Current Balance

$50

Utilization

10%

This low utilization level may contribute positively to many credit scoring models.

Debit cards do not generate utilization ratios because they do not involve credit lines.

Building a Positive Credit Profile

Over time, responsible secured card usage may help establish:

- Positive payment history

- Credit account longevity

- Improved lender confidence

- Better borrowing opportunities

For many people, a secured credit card serves as the first step toward qualifying for traditional unsecured credit cards.

This makes secured cards significantly more effective than debit cards when the goal is building credit.

To better understand the differences, let’s compare both cards side by side.

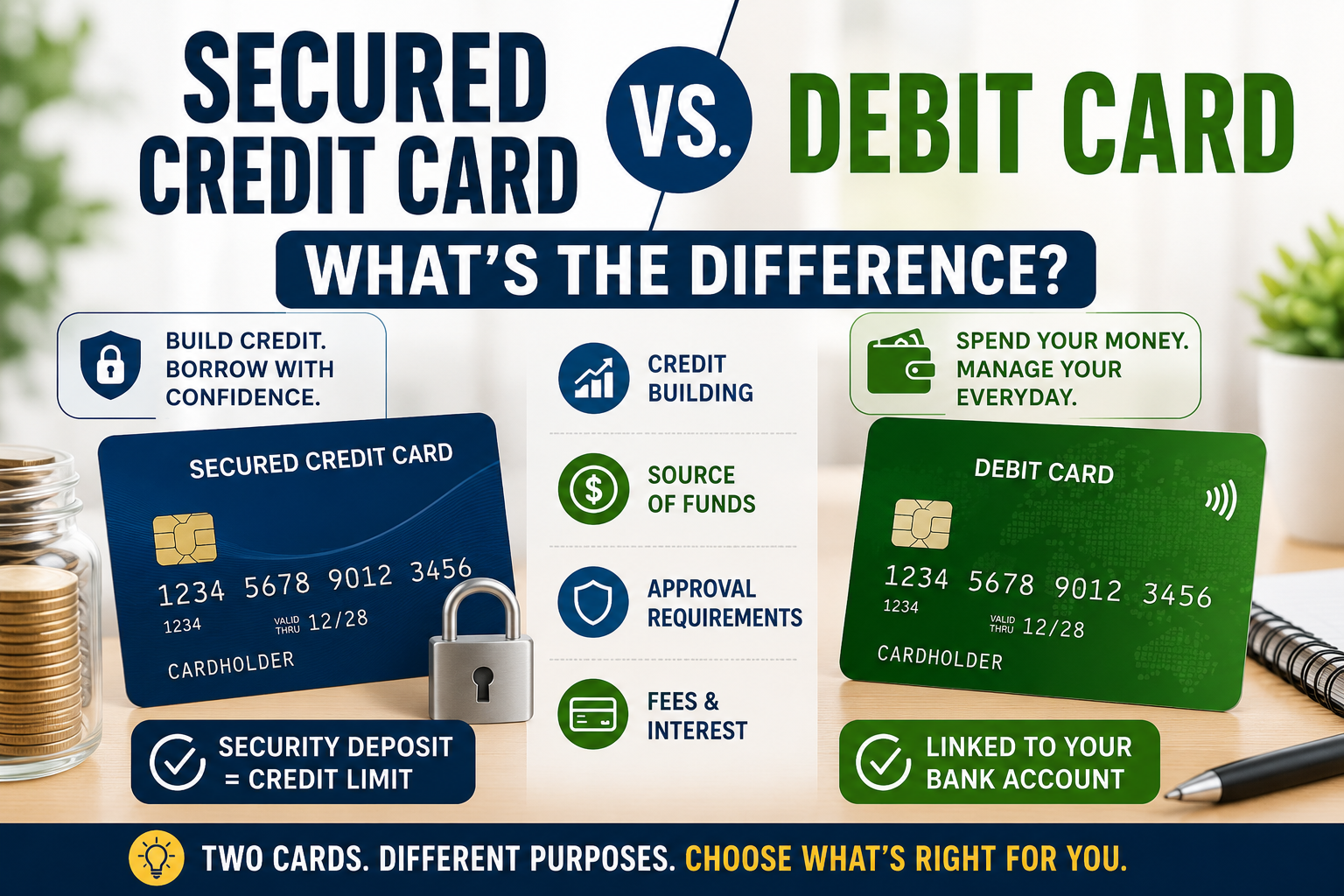

Secured Credit Card vs Debit Card: Side-by-Side Comparison

Although secured credit cards and debit cards may appear similar, their differences become much clearer when viewed directly next to one another.

Source of Funds

Debit Card

Uses money already available in your bank account.

Secured Credit Card

Uses a credit line provided by a lender.

Advantage

Depends on your goal.

Debit cards simplify spending control.

Secured cards provide access to credit-building opportunities.

Credit Building Ability

Debit Card

Generally does not build credit because activity is not typically reported to credit bureaus.

Secured Credit Card

Can help build credit through reported payment history and credit management.

Advantage

Secured credit card.

Approval Requirements

Debit Card

Typically available when opening a checking account.

Secured Credit Card

Requires application approval and a security deposit.

Advantage

Debit card.

Spending Limits

Debit Card

Limited by available account balance.

Secured Credit Card

Limited by assigned credit limit.

Advantage

Depends on personal financial circumstances.

Fraud Protection

Debit Card

Protection exists but may vary depending on issuer and timing of fraud reporting.

Secured Credit Card

Credit cards often provide strong consumer protections and dispute resolution processes.

Advantage

Secured credit card.

Fees

Debit Card

May involve:

- Monthly account fees

- Overdraft fees

- ATM fees

Secured Credit Card

May involve:

- Annual fees

- Interest charges

- Security deposits

Advantage

Depends on the specific products being compared.

Financial Benefits

Debit Card

Helps manage spending and avoid debt.

Secured Credit Card

Helps build credit and establish borrowing history.

Advantage

Depends entirely on your financial goals.

Quick Comparison Summary

| Feature | Debit Card | Secured Credit Card |

| Uses Your Own Money | Yes | No |

| Uses Borrowed Money | No | Yes |

| Builds Credit | Usually No | Usually Yes |

| Requires Security Deposit | No | Yes |

| Requires Repayment | No | Yes |

| Can Improve Credit Score | No | Potentially Yes |

| Risk of Interest Charges | No | Yes |

| Best For | Spending & Budgeting | Building Credit |

The comparison highlights an important truth:

Neither card is universally better.

The right choice depends on what you want to accomplish financially.

The next step is examining the specific advantages and disadvantages of each option so you can determine which tool best fits your personal goals.

Advantages of Debit Cards

Debit cards remain one of the most widely used financial tools in the world.

For many people, they serve as the primary method for making everyday purchases, paying bills, and managing household expenses.

Although debit cards do not typically help build credit, they offer several important benefits that make them valuable for day-to-day financial management.

No Borrowing Required

Perhaps the biggest advantage of a debit card is that it allows you to spend money you already have.

Unlike credit cards, there is no borrowing involved.

When you make a purchase, funds are generally deducted directly from your bank account.

This structure helps many people avoid accumulating debt because they are not spending money they will need to repay later.

For beginners who are still learning money management skills, this can provide an extra layer of financial discipline.

Easier Budgeting

Many people find budgeting easier when using debit cards.

Because spending comes directly from available funds, it is often simpler to track where money is going.

For example:

- Account Balance: $1,000

- Purchase: $100

- Remaining Balance: $900

This immediate visibility can help individuals stay within spending limits and avoid financial surprises.

Many budgeting apps also connect directly to checking accounts, making debit card spending easy to monitor.

Lower Risk of Debt

Debt becomes possible when borrowed money is not repaid promptly.

Since debit cards generally do not involve borrowing, there is less risk of carrying balances and paying interest charges.

This can be especially helpful for individuals who:

- Struggle with overspending

- Prefer simple financial systems

- Want to avoid credit card debt entirely

While debit cards do not eliminate all financial risks, they can reduce the temptation to spend beyond available resources.

Simple Everyday Spending

Debit cards are convenient.

They can be used for:

- Grocery shopping

- Fuel purchases

- Restaurant bills

- Online shopping

- Utility payments

Because they are linked directly to your bank account, they provide quick and easy access to your money.

Many people use debit cards daily without needing to think about billing cycles, interest rates, or credit utilization.

This simplicity makes them appealing for routine transactions.

Real-Life Example

Imagine Sarah receives her paycheck every two weeks and prefers using a debit card for most purchases.

Because every transaction comes directly from her checking account, she always knows how much money remains available.

She avoids debt, stays within budget, and finds money management straightforward.

For someone focused primarily on controlling spending, a debit card may be an excellent financial tool.

However, debit cards also have limitations, particularly when it comes to building credit and creating financial opportunities.

Disadvantages of Debit Cards

While debit cards offer convenience and spending control, they are not perfect.

Understanding their limitations can help you determine whether they fully support your long-term financial goals.

No Credit Building

The biggest drawback of a debit card is that it generally does not help build credit.

This surprises many people.

Someone may use a debit card responsibly for years and still have little or no credit history.

Because debit card activity is not typically reported to major credit bureaus, those transactions do not contribute to traditional credit scores.

As a result, responsible debit card usage alone may not improve your ability to qualify for future credit products.

Limited Financial Growth Benefits

A positive credit history can create access to:

- Credit cards

- Auto loans

- Mortgages

- Better borrowing terms

Because debit cards generally do not help establish that history, they provide fewer long-term credit-building benefits.

Someone who relies exclusively on debit cards may eventually discover that lenders have very little information available to evaluate their borrowing behavior.

Reduced Borrowing History

Lenders prefer evidence that borrowers can manage credit responsibly.

Without credit accounts, there may be little information available regarding:

- Payment history

- Credit utilization

- Borrowing behavior

This lack of data can make it more difficult to qualify for certain financial products.

Even individuals with strong savings habits may face challenges if they have never established a credit history.

Potential Overdraft Risks

Although debit cards help prevent debt in many situations, overdraft fees can still occur.

For example:

- Account balance: $50

- Purchase amount: $75

Depending on account settings and bank policies, the transaction may:

- Be declined

- Trigger overdraft protection

- Generate overdraft fees

Repeated overdrafts can become expensive.

Monitoring account balances carefully remains important.

Real-Life Example

John uses only a debit card because he dislikes borrowing money.

After several years, he applies for a car loan and discovers he has very limited credit history.

Although he has managed his money responsibly, lenders have little information available to assess his ability to repay borrowed funds.

This situation demonstrates why some people choose to combine debit cards with credit-building tools such as secured credit cards.

Let’s examine the benefits secured credit cards can provide.

Advantages of Secured Credit Cards

Secured credit cards were specifically created to help people establish or rebuild credit.

For individuals with limited credit history, they often provide opportunities that debit cards cannot.

Although they require responsible management, secured cards offer several important benefits.

Credit-Building Opportunities

The most significant advantage of a secured credit card is its ability to help build credit.

Most reputable secured card issuers report account activity to major credit bureaus.

This reporting can help establish:

- Payment history

- Account age

- Credit utilization data

- Borrowing history

Over time, these factors may contribute to stronger credit profiles.

For individuals with no credit history, this benefit can be extremely valuable.

Establishing Financial History

Many lenders want evidence that applicants can manage borrowed money responsibly.

A secured credit card provides an opportunity to create that evidence.

Each on-time payment helps demonstrate responsible financial behavior.

Over months and years, this information forms the foundation of your credit profile.

This can make future borrowing opportunities more accessible.

Potential Upgrade Path

Many secured credit cards are designed as stepping stones.

Responsible cardholders may eventually qualify for:

- Unsecured credit cards

- Higher credit limits

- Better rewards programs

- Additional financial products

Some issuers even offer graduation programs that automatically review accounts for upgrades.

This means a secured card may be the beginning of a much broader financial journey.

Financial Education Benefits

Using a secured credit card teaches important financial skills.

Cardholders learn about:

- Payment due dates

- Credit utilization

- Interest charges

- Credit reporting

- Responsible borrowing

These lessons can help prevent costly mistakes later when larger credit limits become available.

Many people view secured cards as practical training tools for long-term credit management.

Real-Life Example

Alex has no credit history and wants to build credit before applying for an apartment.

He opens a secured credit card with a $300 deposit.

For the next year he:

- Makes every payment on time

- Maintains low balances

- Monitors account activity regularly

As a result, he establishes positive credit history and improves his chances of qualifying for future financial products.

Despite these advantages, secured credit cards also come with responsibilities and potential drawbacks.

Disadvantages of Secured Credit Cards

Secured credit cards can be excellent credit-building tools, but they are not the right solution for everyone.

Understanding their limitations helps ensure realistic expectations.

Security Deposit Requirement

The most obvious disadvantage is the required security deposit.

Unlike traditional unsecured credit cards, secured cards require money upfront.

Common deposits include:

- $200

- $300

- $500

- $1,000

While the deposit is generally refundable, it still represents money that cannot be used elsewhere while the account remains open.

For some individuals, saving the deposit can be challenging.

Risk of Interest Charges

Because secured cards are credit products, interest charges may apply if balances are carried from month to month.

For example:

- Balance: $300

- Payment not made in full

Interest may be added according to the card’s terms.

Debit cards do not have this issue because purchases are paid immediately using available funds.

This makes responsible repayment especially important.

Potential Fees

Some secured credit cards charge fees such as:

- Annual fees

- Application fees

- Monthly maintenance fees

Not all secured cards include these costs, but it is important to review terms carefully before applying.

Comparing multiple options can help identify cards with lower overall costs.

Requires Responsible Management

A secured card can help build credit.

However, it can also damage credit if mismanaged.

Common mistakes include:

- Missing payments

- Carrying high balances

- Maxing out credit limits

These behaviors may negatively affect credit profiles.

Unlike debit cards, secured credit cards require ongoing attention and responsible borrowing habits.

Real-Life Example

Emily opens a secured credit card to build credit.

Initially, she uses the card responsibly.

Later, she begins carrying high balances and occasionally pays late.

Instead of improving her credit profile, these habits slow her progress and create additional costs.

This example highlights an important principle:

A secured card can be a powerful financial tool, but only when managed carefully.

Now that we’ve explored the strengths and weaknesses of both options, the next step is determining which card may be the better choice for different types of beginners and financial goals.

Which Is Better for Beginners?

One of the most common questions people ask after learning about debit cards and secured credit cards is:

“Which one should I use?”

The answer depends entirely on your financial goals.

Neither card is universally better.

Each serves a different purpose.

A debit card is primarily a spending and money-management tool.

A secured credit card is primarily a credit-building tool.

Understanding your goals will help determine which option makes the most sense.

If Your Goal Is Managing Spending

A debit card is often the simpler choice.

Because purchases come directly from your bank account, it is generally easier to avoid overspending.

You can only spend money that is available to you.

This makes debit cards attractive for:

- Teenagers learning financial responsibility

- Individuals who prefer cash-flow control

- People recovering from debt problems

- Consumers who want to avoid borrowing

For someone focused primarily on budgeting and controlling expenses, a debit card may provide the structure needed to stay financially disciplined.

If Your Goal Is Building Credit

A secured credit card is usually the stronger option.

Because secured cards report account activity to credit bureaus, they provide opportunities to establish credit history.

This can help with future goals such as:

- Renting an apartment

- Qualifying for a mortgage

- Obtaining an auto loan

- Accessing better credit card offers

Someone who uses only a debit card may manage money responsibly for years without creating a meaningful credit history.

A secured card helps solve that problem.

If Your Goal Is Both

Many people eventually discover they do not need to choose one or the other.

Instead, they use both cards strategically.

A debit card can help with:

- Daily budgeting

- Cash-flow management

- Spending discipline

A secured credit card can help with:

- Credit-building

- Establishing payment history

- Demonstrating responsible borrowing

Combining both tools often provides the greatest overall benefit.

This is why many financial experts recommend using them together rather than viewing them as competitors.

Can You Use Both Together?

Absolutely.

In fact, for many beginners, using both a debit card and a secured credit card is one of the most effective approaches.

Each card performs a different job.

Rather than replacing one another, they often complement each other.

Why Many Financial Experts Recommend Both

Think of these cards as tools in a toolbox.

A hammer and screwdriver are both useful, but they solve different problems.

The same principle applies here.

Debit Card

Best for:

- Accessing your own money

- Daily spending

- Budget control

Secured Credit Card

Best for:

- Building credit

- Establishing borrowing history

- Improving financial opportunities

Using both allows you to benefit from the strengths of each.

Everyday Spending Strategy

Many people choose to make most purchases using their debit card.

This approach:

- Simplifies budgeting

- Reduces debt risk

- Helps maintain spending awareness

At the same time, they use a secured credit card for a few small recurring expenses.

Examples include:

- Streaming subscriptions

- Gas purchases

- Mobile phone bills

These small transactions generate credit activity while remaining easy to manage.

Credit Building Strategy

A common beginner strategy looks like this:

Debit Card

Used for:

- Groceries

- Entertainment

- Household purchases

Secured Credit Card

Used for:

- One or two recurring expenses

- Small monthly purchases

- Credit-building purposes

The secured card balance is then paid in full every month.

This allows the user to build credit while minimizing debt risk.

Real-Life Example

Emma has recently started her first full-time job.

She wants to build credit but worries about overspending.

She decides to:

- Use her debit card for most purchases.

- Use a secured credit card for her monthly streaming service and gas purchases.

Every month, she pays the secured card balance in full.

As a result, she:

- Maintains control of her spending.

- Avoids interest charges.

- Builds positive credit history.

This balanced approach helps her achieve both financial goals simultaneously.

While using both cards can be effective, understanding how real people apply these strategies can provide even greater clarity.

Real-Life Examples

The following examples demonstrate how different individuals may choose between debit cards and secured credit cards based on their financial goals.

Example 1: Student Building Credit

Jordan is a college student with no credit history.

He already has a checking account and uses a debit card regularly.

After learning that debit card activity does not typically build credit, he opens a secured credit card with a $300 deposit.

For the next year he:

- Uses the secured card for small purchases.

- Pays every bill on time.

- Keeps balances low.

As a result, he establishes positive credit history before graduation.

Key Lesson

A debit card helps manage spending, while a secured card helps build credit.

Using both creates a stronger financial foundation.

Example 2: New Worker Managing Money

Sophia recently started her first full-time job.

Her primary concern is staying within budget.

She prefers using a debit card because every purchase comes directly from her account.

However, she also understands the importance of building credit.

She uses a secured card for a single monthly subscription and pays it off immediately.

Key Lesson

You do not need to put every purchase on a secured credit card to build credit.

Small, consistent usage can still provide benefits.

Example 3: Rebuilding Credit After Financial Problems

Carlos experienced financial hardship several years ago and wants to rebuild his credit profile.

Although he uses a debit card for everyday spending, he opens a secured credit card specifically for credit-building.

Over time he:

- Makes every payment on time.

- Maintains low utilization.

- Avoids unnecessary debt.

Gradually, his credit profile improves.

Eventually, he qualifies for an unsecured credit card with better benefits.

Key Lesson

Secured cards can provide a practical pathway toward rebuilding credit after setbacks.

These examples demonstrate that the best choice often depends on your circumstances rather than the card itself.

However, even with the right card, mistakes can slow financial progress.

Understanding common pitfalls can help you avoid unnecessary setbacks.

Common Mistakes to Avoid

Many people make avoidable mistakes when using debit cards and secured credit cards.

Fortunately, most of these mistakes can be prevented through awareness and planning.

Assuming Debit Cards Build Credit

This is one of the most common misconceptions among beginners.

Many people believe that years of responsible debit card usage automatically improve credit scores.

In most cases, debit card activity is not reported to major credit bureaus.

How to Avoid It

If building credit is a goal, consider using a credit-building product such as a secured credit card in addition to your debit card.

Missing Secured Card Payments

Even small missed payments can negatively affect credit-building progress.

A secured card only helps when it is managed responsibly.

How to Avoid It

Consider:

- Automatic payments

- Calendar reminders

- Payment alerts

Consistency is critical.

Carrying High Credit Card Balances

Some beginners mistakenly believe carrying a balance helps build credit.

This is not true.

High balances can increase credit utilization and potentially hurt credit scores.

How to Avoid It

Keep balances low and pay them off whenever possible.

Responsible usage matters far more than carrying debt.

Ignoring Credit Reports

Many consumers focus on using their cards but never review their credit reports.

This can allow errors or fraudulent activity to go unnoticed.

How to Avoid It

Review your credit reports periodically and monitor your accounts regularly.

Awareness helps protect both your credit profile and financial security.

Focusing Only on the Card

Many people believe the card itself will automatically improve their financial situation.

In reality, financial success depends on behavior.

A debit card used irresponsibly can create problems.

A secured credit card used irresponsibly can damage credit.

How to Avoid It

Focus on:

- Responsible spending

- On-time payments

- Financial discipline

- Long-term habits

The card is simply a tool.

Your behavior determines the outcome.

Now that we’ve covered real-world usage and common mistakes, the next step is examining what realistic credit-building progress looks like and how secured credit cards fit into a long-term financial strategy.

Realistic Expectations: Building Credit With a Secured Card

One of the biggest mistakes beginners make is expecting immediate results.

After opening a secured credit card, many people hope their credit score will improve dramatically within a few weeks.

Unfortunately, credit-building rarely works that way.

Like most worthwhile financial goals, building credit takes time, consistency, and patience.

Understanding what realistic progress looks like can help you stay motivated and avoid unnecessary frustration.

First 3 Months

During the first few months, your primary objective is establishing positive account activity.

Focus on:

- Making every payment on time

- Keeping balances low

- Using the card regularly

- Avoiding missed due dates

At this stage, lenders and credit bureaus are beginning to collect information about your account.

You may not see major changes immediately, and that’s completely normal.

The goal during this period is creating a strong foundation.

Months 4–6

After several months of positive activity, your credit profile begins developing more meaningful history.

If you’ve consistently:

- Paid on time

- Maintained low utilization

- Avoided excessive debt

you may begin seeing positive changes.

Many people notice:

- Increased confidence managing credit

- Initial credit score improvements

- Better approval odds for certain financial products

However, progress varies from person to person.

Individuals rebuilding damaged credit may experience a different timeline than someone establishing credit for the first time.

Months 7–12

By this point, lenders have accumulated a larger sample of your borrowing behavior.

Responsible cardholders may begin receiving:

- Higher credit limits

- Pre-approved credit offers

- Graduation opportunities

- Better credit products

For secured credit card users, this period often includes account reviews that may lead to unsecured card eligibility.

The exact timing depends on:

- Card issuer policies

- Payment history

- Credit utilization

- Overall credit profile

Typical Results

Many successful credit-building journeys follow a similar pattern:

Month 1

Learning how credit works.

Month 3

Establishing positive payment habits.

Month 6

Building measurable credit history.

Month 12

Qualifying for stronger financial opportunities.

The most important thing to remember is that consistency matters far more than speed.

Small positive actions repeated month after month often produce significant long-term results.

How This Relates to Secured and Unsecured Credit Cards

By now, you understand the difference between debit cards and secured credit cards.

You also understand how secured cards can help build credit.

The next logical step is understanding how secured cards fit into the broader credit-building journey.

For many people, secured cards are not the final destination.

They are the starting point.

When to Start With a Secured Card

A secured card may be a good choice if:

- You have no credit history.

- You have limited credit history.

- You’ve been denied traditional credit cards.

- You’re rebuilding credit after financial difficulties.

In these situations, secured cards provide an opportunity to establish positive borrowing behavior while minimizing lender risk.

When to Upgrade

As your credit profile improves, you may eventually qualify for unsecured credit cards.

Signs you may be ready include:

- Consistent on-time payments

- Low credit utilization

- Several months of positive account history

- Improving credit scores

Many card issuers periodically review secured card accounts and may offer upgrade opportunities automatically.

The Long-Term Goal

For most people, the goal is not simply obtaining a secured credit card.

The goal is building a strong credit profile.

A strong credit profile can help create opportunities such as:

- Better credit cards

- Lower borrowing costs

- Mortgage qualification

- Auto loan approval

- Greater financial flexibility

The secured card simply helps establish the foundation.

Continue Learning About Credit

If you’re interested in understanding how secured credit cards compare to traditional credit cards, be sure to read our complete guide:

Secured vs Unsecured Credit Cards Explained

That guide explores:

- Approval requirements

- Credit-building potential

- Rewards programs

- Credit limits

- Which option may be best for your situation

Together, these resources provide a comprehensive foundation for understanding beginner credit-building strategies.

Final Thoughts

Although secured credit cards and debit cards may look similar, they serve very different purposes.

A debit card gives you access to money you already own.

A secured credit card gives you access to a credit line that can help establish or rebuild your credit history.

Neither card is inherently better.

The right choice depends on your goals.

If your primary objective is:

- Managing spending

- Avoiding debt

- Accessing your own money

a debit card may be all you need.

If your primary objective is:

- Building credit

- Establishing borrowing history

- Improving future financial opportunities

a secured credit card may be the better choice.

For many people, the most effective solution is using both cards together.

A debit card can help manage daily spending while a secured credit card helps build a positive credit profile.

The key takeaway is simple:

The card itself is only a tool.

Your financial habits ultimately determine your success.

Paying bills on time, spending responsibly, monitoring accounts, and maintaining good financial discipline will always matter more than the type of card you carry.

By understanding how these financial tools work and using them strategically, you can make more informed decisions and build a stronger financial future.

Frequently Asked Questions

Is a secured credit card the same as a debit card?

No. A debit card uses money already available in your bank account, while a secured credit card uses a credit line provided by a lender. Although secured cards require a security deposit, purchases are made using borrowed funds that must be repaid. This borrowing activity can help build credit when managed responsibly.

Which is safer: a debit card or a secured credit card?

Both can be safe when used properly. Debit cards reduce the risk of debt because you spend your own money. Secured credit cards often provide stronger credit-building opportunities and may offer additional consumer protections. The safer option depends on your financial habits and goals.

Can a debit card improve my credit score?

Generally, no. Debit card transactions are usually not reported to major credit bureaus because they do not involve borrowing money. As a result, responsible debit card usage typically does not contribute directly to your credit score.

Why do secured credit cards require deposits?

The deposit reduces lender risk. It serves as collateral if the borrower fails to repay borrowed funds. Because of this protection, lenders are often willing to approve applicants who have little or no credit history.

Should students use secured credit cards?

Many students benefit from secured credit cards because they provide an opportunity to establish credit history early. Responsible usage can help students build positive financial habits and prepare for future borrowing needs.

Can I use a secured card like a debit card?

Yes, many people use secured cards for small everyday purchases. However, unlike a debit card, the balance must be repaid later. Treating a secured card like a debit card by spending only what you can afford to repay is often a smart strategy.

Is a secured card worth it for building credit?

For many people, yes. A secured credit card is often one of the easiest ways to establish or rebuild credit. When payments are made on time and balances remain low, secured cards can contribute positively to credit-building efforts.

Can I have both a debit card and a secured credit card?

Absolutely. Many people use a debit card for daily spending and a secured credit card for credit-building purposes. This combination allows them to enjoy the advantages of both tools.

What happens if I miss a secured card payment?

Missing a payment may result in fees, interest charges, and potential damage to your credit profile. Payment history is one of the most important factors in credit-building, making on-time payments extremely important.

How long should I keep a secured credit card?

Many people keep secured cards until they qualify for unsecured credit cards. Depending on the issuer and your financial behavior, this may take several months or several years. The best timeline depends on your personal credit-building progress.